Telecom debt collection focuses on recovering unpaid bills from services like mobile, internet, and landlines. With 450 million post-paid wireless accounts in the U.S. and $3 billion in past-due balances, it's a major challenge for providers. Key points:

- Delinquency rates: 1–5% of accounts fall behind, with balances averaging $200–$300.

- Unique challenges: Telecom debt often isn’t reported until it goes to collections, making recovery harder.

- Sources of debt: Missed payments, surprise charges, early termination fees, and unpaid equipment costs.

Modern Strategies for Better Results

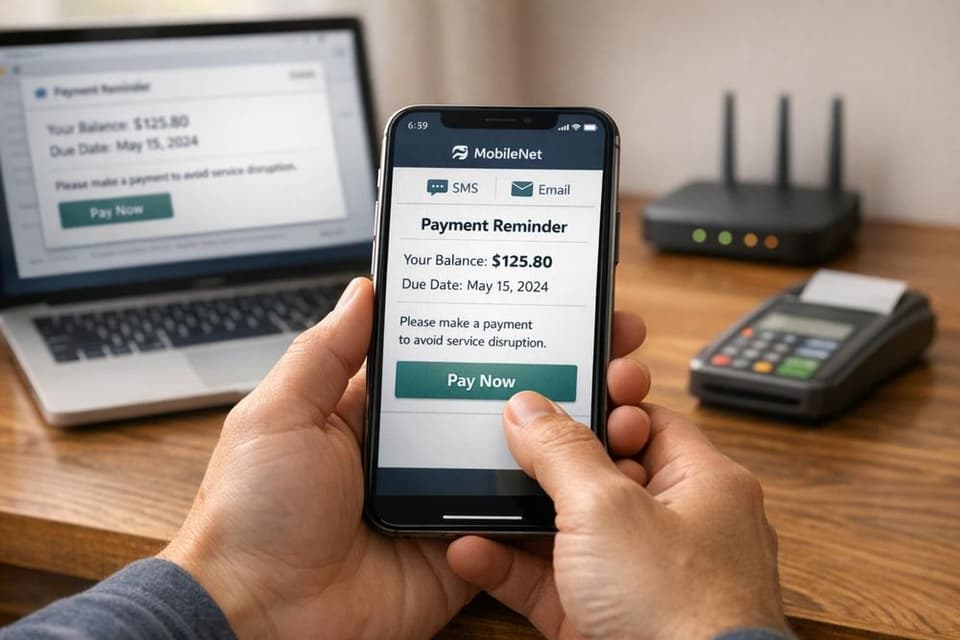

Traditional call-based methods are being replaced by digital-first approaches, like SMS and email reminders. For example, providers using AI-driven platforms have seen up to a 35% increase in recovery rates.

- Key tools: Omnichannel outreach, predictive analytics, and self-service payment portals.

- Preferred methods: 73% of Gen Z prefers SMS reminders, with SMS response rates at 45%.

Compliance and Security

Strict regulations like the TCPA and CFPB’s 7-in-7 rule govern contact frequency and methods. Collectors must also secure customer data with encryption and follow opt-out requests to avoid penalties.

Metrics That Matter

Success is measured by metrics like Days Sales Outstanding (DSO), Collection Effectiveness Index (CEI), and broken Promise to Pay rates. These help optimize strategies and improve recovery rates, which currently average just 20%.

Telecom debt collection is evolving. By using advanced tools and meeting compliance standards, providers can recover more while keeping customer relationships intact.

Telecom Debt Collection Statistics and Recovery Strategies

Telecom Debt Collection Statistics and Recovery Strategies

Revolutionizing Debt Collection | The Power of Self-Service Portals | Ep. 211

What Makes Telecom Debt Different

Telecom debt stands apart from other types of consumer debt due to its unique characteristics. Unlike credit cards or auto loans, which typically report monthly payment activity, telecom providers usually only report accounts once they’ve gone into collections. This means that nearly 95% of telecom-related items on credit reports appear as collection entries, not active account histories.

The structure of telecom debt also creates specific challenges. With a median balance of $408 per account, telecom debts are often low in value but high in volume. Between mid-2013 and early 2018, 22% of consumer credit reports included at least one telecom-related collection item, and around 17% of these balances exceeded $1,000. Given these dynamics, effective segmentation and automation are critical for managing recovery efforts.

"The threat of turning off a customer's service no longer carries any weight, as they will simply switch to another provider." - Credence Global Solutions

The mobility of telecom customers further complicates debt recovery. Unlike landline debts, which are tied to a fixed address, mobile service users frequently move or switch providers. This makes locating them - often referred to as skip-tracing - more difficult. Traditional methods, like disconnecting service, are no longer effective because customers can easily switch to a competitor. Some providers even offer incentives to cover termination fees, reducing the consequences of unpaid bills. These issues demand advanced tools and strict compliance measures, which will be discussed in later sections.

Common Sources of Telecom Debt

Telecom debt stems from several key sources:

- Unpaid service charges: Missed monthly payments often form the foundation of telecom debt.

- Unexpected charges: "Surprise bills" arise when consumers exceed data limits, incur roaming fees, or misunderstand contract terms. These charges can quickly add up to hundreds of dollars.

- Early termination fees (ETFs): In a competitive market, customers often leave contracts early to join new providers, leaving ETFs unpaid as they focus on their new services.

- Equipment-related debt: This includes unpaid installment plans for high-value devices like smartphones or charges for unreturned leased equipment after a contract ends.

Regulatory Requirements

Telecom debt collection operates within a strict regulatory framework, adding another layer of complexity. Key regulations include:

Telephone Consumer Protection Act (TCPA) of 1991: This law limits the use of robocalls, prerecorded messages, and automatic dialing systems, especially for wireless phones. Collectors must ensure they have proper consent and train staff to comply.

FCC's "Red Light Rule": This rule prevents the Federal Communications Commission (FCC) from processing applications for licenses or benefits from entities with outstanding non-tax debts. It matches a debtor’s Taxpayer Identification Number (TIN) with their FCC Registration Numbers and dismisses applications if delinquencies are found.

Debt Collection Improvement Act (DCIA) of 1996: Under this act, unpaid invoices issued by the Universal Service Administrative Company (USAC) are treated as debts owed to the U.S. government. These debts are automatically referred to the Department of Treasury for collection.

CFPB's "7-in-7" Rule: This rule limits debt collectors to no more than seven calls to a debtor about a specific debt within seven consecutive calendar days. Violating this rule could result in regulatory penalties.

How to Evaluate and Acquire Telecom Debt Portfolios

Navigating the world of telecom debt portfolios requires a structured approach to identify opportunities while minimizing risk. With over $3 billion in past-due debt in the U.S. telecom market, there’s no shortage of portfolios available. However, since unpaid debts can cost telecom operators up to 2% of their annual revenue, careful evaluation is essential before making any acquisitions.

"There's no such thing as 'bad debt,' only bad pricing." - Jeffery Hartman, Director of Portfolio Liquidity & Asset Disposition, DebtLink

Debt pricing varies significantly based on the portfolio type. For example, performing debt trades at $0.25–$0.45+ per dollar, fresh charge-offs sell for $0.03–$0.10 per dollar, and out-of-statute accounts are priced as low as $0.001–$0.01 per dollar. Knowing these benchmarks ensures buyers avoid overpaying while sellers can price portfolios competitively. This pricing knowledge forms the foundation for effective portfolio segmentation.

Portfolio Segmentation Methods

Breaking down portfolios into meaningful segments is a key step in evaluating their potential. Start by categorizing accounts based on their delinquency stage: early delinquency (30+ days), advanced delinquency (60–120 days), and legal action stages (more than 120 days). Advanced analytics tools, such as Random Forest and XGBoost, can predict which accounts are likely to resolve on their own versus those requiring intervention.

Segmentation also depends on four key data types:

- On-us behavior: Includes payment history and returned checks.

- Off-us behavior: Draws from credit bureau data and telecom-specific records.

- Previous contact history: Looks at response rates and broken promises.

- Socio-demographic data: Factors like age, location, and digital literacy.

For instance, 73% of Gen Z consumers prefer SMS reminders for payments, suggesting that portfolios with younger debtors might benefit from digital-first collection strategies. Testing different collection flows through champion/challenger testing can further refine segmentation strategies and boost ROI.

Risk Assessment and Valuation

Once segmented, portfolios undergo a thorough risk assessment to refine their valuation and guide acquisition decisions. This process starts with examining the account lifecycle, focusing on key dates such as the open date, last payment date, and charge-off date. Accounts with longer gaps between the last payment and charge-off are often harder to recover. Geographic distribution also plays a role, as states with shorter statutes of limitations can restrict legal recovery options like garnishments or judgments.

Accurate data is critical for valuation. For example, skip trace hit rates - measuring how often updated contact information is successfully found - can reveal the quality of the portfolio's data. It’s also important to check whether the portfolio has been worked by an agency or in-house before, as well as its historical liquidation data. Portfolios with poor data integrity or multiple prior collection attempts often command lower bids.

Using historical liquidation data and predictive models can help estimate recovery rates and set competitive bid levels. Advanced analytics, for instance, can improve recovery rates by up to 10% compared to older static scorecard methods. During valuation, calculate key metrics such as:

- Gross yield: Total recovery compared to purchase price.

- Right party contact (RPC) rate: Success in reaching the correct debtor.

- Liquidation percentage: Percentage of the debt recovered.

- Settlement rate: Frequency of negotiated settlements.

Before finalizing an acquisition, verify the portfolio's resale flexibility. Check whether the paper can be resold, if lender approval is needed, and whether uncollectible accounts (e.g., due to bankruptcy, fraud, or deceased debtors) can be returned. These steps ensure you’re not only acquiring a portfolio but also setting yourself up for success.

Collection Techniques for Telecom Debt

Recovering funds in the telecom industry requires strategies that are both effective and adaptable. While the average recovery rate hovers around 20%, using the right techniques can push this number much higher. Success often hinges on aligning collection strategies with the digital communication habits identified during portfolio evaluations. This approach not only enhances recovery efforts but also sets the groundwork for proactive measures that help customers stay informed and avoid missed payments.

Prevention Through Clear Communication

The best way to manage collections is to prevent overdue payments in the first place, and that starts with clear, upfront communication. Service agreements should clearly outline payment terms, late fees, and disconnection policies to eliminate confusion from the beginning. Detailed billing statements that break down usage and upcoming charges also help customers understand exactly what they owe.

Automated reminders - sent 3 to 7 days before a payment is due - via SMS, email, or app notifications have been shown to prompt about 23% of late-paying customers to pay on time. These reminders work because they are proactive and non-threatening. For example, an Indian telecom provider cut its Days Sales Outstanding (DSO) by 20% and achieved a Collection Effectiveness Index (CEI) of 88% by combining automated reminders with flexible payment plans and empathetic follow-ups.

"The same provider maintained an 85% Customer Satisfaction Score even during collections by offering multilingual support and treating customers as partners."

Multi-Channel Outreach Methods

Relying solely on traditional call centers is no longer as effective as it once was. Declining right-party contact rates and high staffing costs have made this approach less practical. Instead, a digital-first, omnichannel strategy meets customers where they already are. For instance, SMS messages have a 98% open rate and a 45% response rate - far surpassing email's 20% open rate and 6% response rate. In fact, debtors are 134% more likely to respond to SMS than email, and 85% prefer receiving texts over phone calls.

Major U.S. telecom providers have seen significant improvements in liquidation rates by adopting digital-first strategies over traditional call-and-collect methods. Combining SMS, email, WhatsApp, Facebook Messenger, and AI-driven chatbots creates multiple touchpoints, making it easier for customers to engage. Each message should include a direct link to a secure payment portal, enabling quick and easy transactions. Advanced analytics can further refine this approach by identifying the best message, timing, and channel for each customer based on their behavior and preferences. This is especially important for younger audiences, with 73% of Gen Z consumers naming SMS as their preferred method for receiving payment reminders.

Payment Plans and Settlement Options

It's important to remember that not all delinquent customers are unwilling to pay - many simply can't pay the full amount right away. While using multiple communication channels improves contact rates, offering flexible payment options is just as critical. Structured payment plans tailored to a customer’s financial situation can help both parties find a workable solution. These plans should consider factors like the cause of delinquency, the duration of financial hardship, and the customer’s disposable income.

Other options, like service plan downgrades or short-term payment deferrals, can prevent total disconnection while keeping the customer relationship intact. Self-service portals that allow customers to set up payment arrangements on their own, at any time, reduce the friction and embarrassment often associated with collections. For cases requiring negotiation, training staff in empathetic communication and financial literacy can lead to better outcomes.

"Showing empathy during your borrowers' financial hardships can help you build trust in the relationship and create an environment where collaborative solutions for overdue payments can be explored together" - Temenos

Early-stage delinquencies can often be resolved with gentle reminders, while more intensive strategies, like negotiations or service suspensions, should be reserved for customers who remain unresponsive. For those who genuinely cannot pay, referring them to debt counseling services rather than pursuing aggressive collection efforts can preserve goodwill and improve the chances of recovery when their financial situation improves.

Technology Tools for Telecom Debt Collection

Modern technology is reshaping the way telecom providers handle overdue accounts. By automating tasks and tailoring communication strategies, advanced platforms simplify workflows and enable smarter decision-making.

Centralized Collection Platforms

Managing collections with scattered spreadsheets and disconnected systems can be chaotic. Centralized platforms solve this by providing a real-time view of every account, automating communications based on account changes, and reserving the most complex cases for human agents. This approach drastically reduces manual effort.

For example, Provenir uses machine learning models like Random Forest and XGBoost to create personalized collection strategies for wireless carriers. Meanwhile, CGI Credit Studio offers low-code tools that let business users tweak collection rules without waiting for IT support. Symend takes a unique approach by combining behavioral science with AI to recover debts while maintaining positive customer relationships.

These platforms excel in intelligent segmentation. Instead of processing accounts in a fixed order, they categorize customers based on factors like "capacity to pay" and "readiness to pay." This helps teams focus on high-priority accounts. Real-time data syncing through REST APIs and SFTP ensures that billing and CRM systems stay updated, reducing disputes caused by outdated information.

"Telcos that deploy advanced analytics to get ahead of payment risks see up to a 10% improvement in recovery rates when compared to those who use legacy processes and static scorecard methods." - Michael Fife, VP Sales & Consulting, US, Provenir

Centralized data management also paves the way for smoother payment experiences.

Payment Gateway Integration

Integrating secure payment systems directly into collection workflows makes it easier for customers to settle their debts. Self-service portals allow users to set up payment plans at any time, reducing the need for agent involvement by as much as 60–85%. Tools like Tratta offer white-label portals with automated email and SMS campaigns, guiding customers to secure payment links for quick, hassle-free transactions.

Platforms like FICO Customer Communication Services automate communication across multiple channels - SMS, email, and voice - while secure IVR systems let customers make payments or set up plans over the phone without speaking to an agent.

These systems adhere to strict security protocols, including end-to-end encryption, tokenization of sensitive data, and PCI DSS Level 1 certification. They also maintain detailed audit logs, enhancing transparency for both disputes and regulatory requirements.

Beyond simplifying transactions, advanced analytics are key to refining collection strategies.

AI and Predictive Analytics

AI tools analyze customer data to predict payment behaviors, shifting the focus from alphabetical account processing to prioritizing accounts based on the likelihood of payment. For instance, TrueAccord uses machine learning to replace traditional call-and-collect methods. Telecom providers using this platform have seen up to a 35% boost in liquidation rates compared to older approaches.

AI also identifies irregular payment patterns, reduced service usage, or frequent credit inquiries, helping teams determine the best time, method, and message to engage with customers.

Fraud detection is another critical application. AI models analyze data to separate fraudulent accounts from legitimate ones, ensuring resources are focused on recoverable debts. As Fernando Lopez, Senior Director of Sales at FICO, explains:

"Fraud is by definition uncollectible... any effort spent to collect on fraudulent accounts is wasted and better used collecting late payments or looking after good customers." - Fernando Lopez, Senior Director of Sales, FICO

Chatbots and conversational AI further enhance efficiency by handling routine negotiations, payment arrangements, and hardship scenarios. These tools provide customers with a private, non-confrontational way to resolve their debts while ensuring compliance with regulations like Reg F and TCPA. Modern AI-powered platforms have been shown to improve recovery rates by 10–15% while cutting operational costs by 40–60%.

Compliance and Data Security

Telecom debt collection operates under strict federal regulations, where non-compliance can lead to hefty penalties. Keeping up with these rules is essential for maintaining lawful and effective collection practices.

Legal Compliance Requirements

Regulation F (12 CFR Part 1006), which enforces the Fair Debt Collection Practices Act (FDCPA), lays out clear guidelines for how collectors can interact with consumers. This includes rules about communication timing, frequency, and the information that must be shared during these interactions.

One key aspect is the 7-7-7 rule: collectors cannot call more than seven times within seven days or follow up within seven days after a conversation. Additionally, collectors must send a validation notice within five days of the first contact. This notice must include the debt amount, the creditor's name, and a statement about the consumer's right to dispute the debt within 30 days. The Consumer Financial Protection Bureau (CFPB) provides sample forms to ensure all required details are included.

Timing matters as well. Collectors can only reach out between 8:00 AM and 9:00 PM in the consumer's local time zone. Contacting them outside these hours could be considered harassment. Voicemails should follow the "limited-content message" format, which avoids revealing sensitive debt collection details. These messages should only include the business name (without indicating debt collection), a request for a callback, the contact person's name, and a return phone number. This approach minimizes the risk of unauthorized third-party disclosures.

"A debt collector may not engage in any conduct the natural consequence of which is to harass, oppress, or abuse any person in connection with the collection of a debt." - Fair Debt Collection Practices Act, Section 806

For emails and texts, Regulation F mandates clear opt-out options and safeguards against third-party exposure. Penalties for violating the FDCPA can reach $1,000 per individual case, and class action damages are capped at $500,000 or 1% of the collector's net worth, whichever is less. State laws often impose stricter standards than federal rules, so it’s crucial to check the specific requirements where you operate.

| Requirement Category | Compliance Standard | Reference |

|---|---|---|

| Call Frequency | Maximum 7 calls in 7 days; 7-day cool-off after a conversation | 12 CFR § 1006.14(b) |

| Contact Hours | 8:00 AM to 9:00 PM (consumer's local time) | 15 USC 1692c |

| Validation Notice | Must be sent within 5 days of first contact | 15 USC 1692g |

| Disputed Debts | Stop collection until verification is mailed to the consumer | 15 USC 1692g |

| Voicemail Format | Use limited-content messages to maintain privacy | 12 CFR § 1006.2(j) |

Once communication rules are addressed, the next priority is safeguarding data.

Data Protection Practices

Beyond compliance, securing consumer data is critical for building trust and meeting regulatory expectations. Strong data protection measures include regular audits and strict controls over information handling. Regulation F also requires collectors to retain records of their activities, as these are subject to CFPB supervision and examination.

Automated systems can help ensure compliance with the seven-calls-in-seven-days rule by tracking call frequency and enforcing cooling-off periods after conversations. Detailed audit logs are equally important for resolving disputes and passing regulatory reviews.

If a consumer requests that all communications stop, collectors must immediately comply. After receiving written notification, contact is only allowed to acknowledge the request or inform the consumer of specific legal actions. Additionally, if the consumer is represented by an attorney, all correspondence must go through that attorney unless they fail to respond within a reasonable time.

The "bona fide error defense" offers limited protection against unintentional violations. To use this defense, collectors must prove that the error occurred despite having robust procedures in place to prevent such issues. This requires presenting evidence that safeguards were actively maintained.

Measuring Performance and Making Improvements

When it comes to telecom debt collection, tracking performance is all about using the right metrics to guide better decisions. Metrics like Days Sales Outstanding (DSO) are key. DSO measures how quickly you turn sales into cash by dividing total accounts receivable by total credit sales, then multiplying by the number of days in the period. A lower DSO means faster cash flow, but it can sometimes be skewed by sudden sales surges. That’s where the Collection Effectiveness Index (CEI) steps in. CEI focuses on the percentage of receivables collected during a set time frame, with scores above 95% indicating strong collection performance. Unlike DSO, CEI zeroes in on the quality of collections.

Another essential metric is Average Days Delinquent (ADD), which tracks how long invoices stay overdue. This number helps you understand whether your collection efforts are speeding up or slowing down. The cost per dollar collected is another critical measure, showing how much you’re spending (on labor, technology, legal fees, etc.) to recover funds. Lastly, the bad debt write-off rate highlights the percentage of receivables deemed uncollectible, offering a direct view of credit risk and collection issues.

Telecom-specific metrics like Promise to Pay (PTP) rates and broken PTP percentages are also important. A high broken PTP rate - when customers fail to follow through on their payment promises - might suggest the need for better negotiation strategies or more flexible payment options. Additionally, tracking dispute resolution time can provide insight into how quickly billing issues are resolved, which directly impacts how fast you can collect payments.

Collection Performance Metrics

Real-world data from three major U.S. telecom providers shows how effective digital-first strategies can be. On average, only 20% of delinquent account balances are recovered, leaving a lot of room for improvement. Considering that U.S. household debt surpassed $18 trillion in Q3 2025 and the average age of debt in collections is roughly 3.5 years, these benchmarks help you evaluate your performance.

| Metric | Formula | What It Reveals |

|---|---|---|

| DSO | (Total AR / Total Credit Sales) × Days in Period | Speed of cash recovery |

| CEI | [(Beg. AR + Sales - End. Total AR) / (Beg. AR + Sales - End. Current AR)] × 100 | Collection efficiency |

| Cost per Dollar | Total Collection Costs / Total Amount Collected | Cost-effectiveness |

| Broken PTP Rate | (Number of Broken PTPs / Total PTPs Made) × 100 | Debtor commitment reliability |

Using Data to Refine Collection Strategies

The real power of these metrics lies in how they can shape smarter collection strategies. For instance, portfolio segmentation allows you to analyze customer data alongside digital response rates, helping you identify patterns like preferred channels for communication. A UK lender found that 90% of customers who opened a collection SMS accessed a self-service portal, and 50% of those scheduled a payment. Insights like these let you focus resources on the most effective channels.

Predictive risk scoring is another game-changer. By using machine learning to analyze customer data, you can predict which accounts are at risk of defaulting and act before they reach advanced delinquency stages. For example, a Middle Eastern telecom operator worked with Subex to analyze handset sales defaults. They discovered that most defaulters were migrant customers, which led to tailored credit policies and repayment plans, ultimately reducing bad debt risk.

"Telcos that deploy advanced analytics to get ahead of payment risks see up to a 10% improvement in recovery rates when compared to those who use legacy processes and static scorecard methods." - Michael Fife, Sam Rohde, and Andy Beddoes, Provenir

Controlled experiments, like champion-challenger testing, can also fine-tune your strategies. These tests compare different dunning sequences to identify the most effective communication methods. Smart dashboards can reveal trends, such as geographic areas with higher default rates, helping you allocate resources more strategically. With up to 5% of U.S. subscriber accounts in delinquency at any given time, even small gains in recovery rates can lead to substantial revenue boosts.

Finally, automation plays a huge role in keeping things moving. By analyzing data from every interaction, you can continuously refine your collection processes. For example, automated reminders have been shown to prompt timely payments in nearly 25% of late cases. Behavioral monitoring can also flag potential issues, such as irregular payment patterns or frequent extension requests, allowing you to intervene before a payment failure occurs. These tools ensure your collection efforts remain efficient and adaptable.

Conclusion

The landscape of telecom debt collection has evolved, requiring smarter strategies, advanced technology, and strict adherence to compliance standards. The old "call-and-collect" methods are quickly becoming obsolete. Instead, digital-first omnichannel outreach has proven effective, increasing liquidations by 32%–35% and catering to 73% of Gen Z consumers who prefer SMS reminders. With over $3 billion in overdue telecom debt at risk in the U.S. and recovery rates averaging just 20%, adopting modern approaches is no longer optional - it's critical.

Transitioning from static scorecards to AI-driven decision-making can improve recovery rates by as much as 10%. Tools like real-time portfolio segmentation, champion–challenger testing, and integrated data analysis - combining customer behavior with third-party credit information - allow for personalized strategies that not only enhance recovery but also maintain positive customer relationships. These advancements also provide a foundation for meeting compliance requirements.

Compliance is non-negotiable in this field. With 100,000 mobile numbers reassigned daily and TCPA fines reaching $1,500 per willful violation, automated number-scrubbing tools and access to the FCC's Reassigned Numbers Database are essential. Platforms must also respect opt-out requests, adhere to approved contact hours, and maintain detailed audit trails to ensure regulatory compliance.

To succeed, debt buyers and sellers should focus on early intervention through pre-collections, automate decisions to concentrate on high-value accounts, and offer self-service portals that align with consumer expectations. Debexpert provides a robust platform for evaluating, acquiring, and managing telecom debt portfolios, complete with built-in analytics and secure communication tools. By combining these strategies with continuous monitoring and iterative improvements, organizations can optimize returns while navigating the complexities of telecom debt management.

FAQs

When should a telecom account be sent to collections?

When a telecom account becomes overdue and initial efforts like reminders and follow-ups fail to resolve the issue, it’s time to consider sending the account to collections. This usually happens 30 to 90 days past due, depending on the company's policies.

Before taking this step, it’s crucial to review a few key factors: the account's payment history, any billing disputes, and the outcome of previous communication attempts. This ensures that moving to collections is the right choice while still aiming to preserve the customer relationship whenever possible.

What data should a buyer require before pricing a telecom debt portfolio?

When purchasing a portfolio, it's crucial to gather detailed information about its key aspects. This includes understanding its origin, structure, risk factors, and historical performance, as well as gaining insights into the debtor profiles.

Pay attention to specific details such as:

- Contact accuracy: Ensure the provided contact information is up-to-date and reliable.

- Credit standing and scores: Review the creditworthiness of the accounts included.

- Recent activity: Look at recent transactions or behaviors to assess portfolio trends.

These elements are critical for determining an accurate price and evaluating the portfolio's potential value.

How can collectors use SMS and self-service portals without breaking TCPA or Reg F?

Collectors can rely on SMS and self-service portals while staying within the boundaries of TCPA and Regulation F by securing clear consumer consent, offering an easy way to opt out, and adhering to time limits (generally 8 AM to 9 PM based on the consumer's local time). Automated messages must also follow these consent and opt-out guidelines. It’s crucial to honor consumer preferences quickly to prevent any compliance issues.