Sell Your Equipment Finance Portfolio

Debexpert connects equipment finance lenders with 100+ verified buyers in a live online auction. Performing loans, deficiencies, non-performing accounts — we sell all types.

100+

Verified equipment finance buyers in the network

$0

Free for sellers — no commissions, no fees

700+

Debt portfolios sold on the platform per year

14–21

Average days from submission to payment

Trusted by over 100 Equipment Finance and BHPH dealers.

You know that getting the best price for your Equipment Finance accounts could be easier, but you're not sure how to do it.

How can you make your Equipment Finance accounts more attractive to buyers?

How can I increase the number of buyers interested in my accounts?

How can I solve the problem of long price negotiations?

Equipment finance lenders face a specific challenge: the buyer pool for non-performing and deficiency accounts is narrow. Most companies either hold the paper indefinitely or accept a single buyer's below-market offer — with no way to know if it's fair.

Debexpert fixes this by putting your portfolio in front of multiple qualified buyers at the same time. They compete. You choose the best offer. That competition is the difference between a lowball and a market price.

All Types of Equipment Finance Paper. One Platform.

Whether you hold a clean book of performing leases or a mixed portfolio with skips, deficiencies, and charge-offs — Debexpert has active buyers for every category.

Performing loans and leases

Active accounts with regular payment history. Highest buyer demand. Ideal for forward flow agreements with fixed, predictable pricing on future originations.

Deficiency accounts

Post-repossession balances where equipment sale did not cover the full amount. Specialist buyers on Debexpert focus exclusively on equipment deficiency recovery.

Non-performing loans

Accounts 90+ days past due. Buyers with established collections and legal recovery infrastructure bid competitively for non-performing equipment finance paper.

Charged-off portfolios

Paper removed from the balance sheet. Debexpert has completed equipment finance transactions from $107K to $121M in face value — single accounts and bulk portfolios.

Why Equipment Finance Lenders Choose Debexpert Over a Single Buyer

The traditional route: approach one buyer, get one offer, take it or leave it. You have no leverage and no way to know if the price reflects the market.

Debexpert runs a competitive auction. Multiple verified buyers bid simultaneously. You see every bid in real time. You choose the winner. That's the difference.

Single debt buyer

- Buyers competing: 1

- Price discovery: Take-it-or-leave-it

- Transparency: None

- Cost to seller: Sometimes commission

- Time to close: Weeks to months

- Documentation: Manual, offline

- Account manager: No

Debexpert auction

- Buyers competing: 100+

- Price discovery: Competitive bidding

- Transparency: Full bid visibility in real time

- Cost to seller: Always free

- Time to close: 14–21 days

- Documentation: End-to-end encrypted drive

- Account manager: Dedicated, throughout the process

How to Sell Your Equipment Finance Portfolio on Debexpert

Six steps from first contact to payment in your account.

Submit your portfolio

Contact your Debexpert account manager. Share the basic details: portfolio size, equipment types, geographic mix, and performing vs. non-performing split. Takes 15 minutes. Costs nothing.

Free portfolio analysis

Our team reviews your data and recommends how to segment the portfolio for maximum bids — by equipment type, account age, collateral status, and geography. We also recommend the optimal auction format: English, Dutch, sealed-bid, or hybrid.

Prepare your masked file and documents

We guide you through creating a masked data file — account-level data with debtor PII protected for pre-bid buyer review. Loan documents, UCC filings, and repossession records are uploaded to Debexpert’s end-to-end encrypted drive.

Presale — buyers review your portfolio

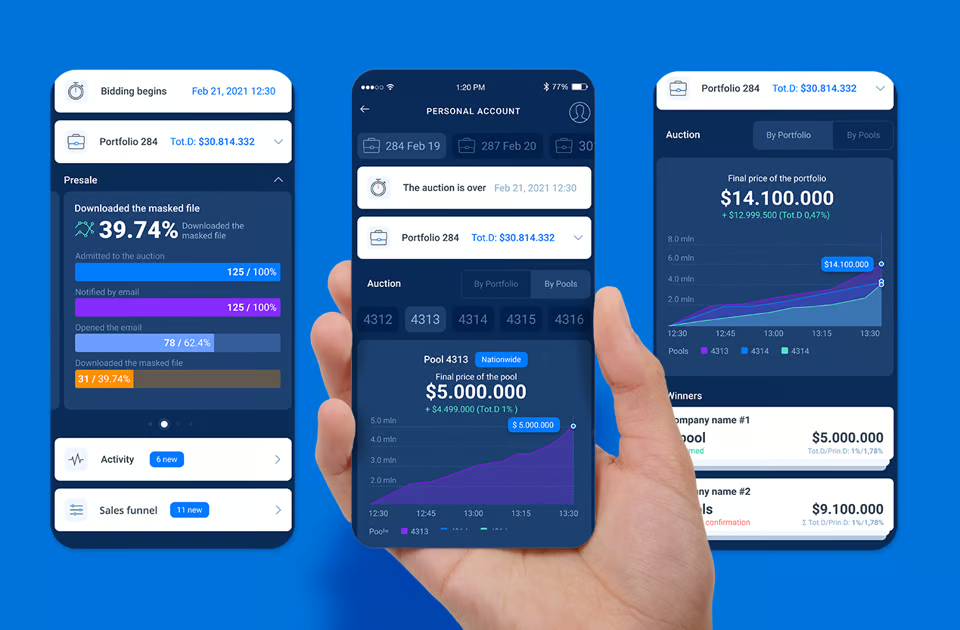

Before the auction opens, Debexpert contacts the most suitable buyers from our network and sends them your masked file. You track who has viewed the portfolio and who has expressed interest — all in your dashboard, in real time.

Live auction — bids come in

Qualified buyers place their bids. You see every bid as it arrives. You communicate directly with buyers through the platform’s secure chat. When the auction closes, you review all offers and select the winner.

Close online and receive payment

The winning buyer signs the Purchase and Sale Agreement directly on the platform. Payment flows from the buyer to you — Debexpert does not hold funds. File transfer happens through the encrypted drive. You’re done. The buyer takes over all collection risk and activity.

5 Reasons to Sell Your Equipment Finance Portfolio Rather Than Hold It

Immediate cash — deploy capital into new originations

Holding a non-performing portfolio means capital is locked and not generating returns. Selling converts that illiquid paper into immediate working capital you can redeploy into new loans, new clients, and new growth.

Transfer all collection risk to the buyer

Once you sell, the buyer assumes every obligation — garnishments, repossession proceedings, legal recovery, and FDCPA compliance. Your team stops spending time and budget on accounts that may never pay.

Competitive bidding drives your price up

When you negotiate with one buyer, they know you have no alternative. When 100+ buyers compete on Debexpert, the final price reflects what the market actually believes your portfolio is worth — not what a single buyer is willing to pay to protect their margin.

Equipment finance paper depreciates — act before it does

Non-performing equipment loans lose value over time. Collateral depreciates. Debtors' assets become harder to trace. The sooner you sell, the more you recover. Waiting costs you money.

Free your team for revenue-generating work

In-house collection on equipment deficiencies and non-performing loans consumes your team's time on accounts that may never recover. Selling the portfolio instantly redirects that capacity to new originations, new clients, and growing the book.

Debexpert takes all the burden off your shoulders, allowing you to sell any Equipment Finance accounts at the highest price in three steps:

Present your Equipment Finance to the market in the best possible light

Debexpert will advise you on how to improve the presentation of your portfolio to increase investor engagement and outcomes for your company. Drawing on our many years of sales experience, we will suggest what information to add to enhance your sales results.

Use our nationwide database of over 100 investors

By offering your skips, deficiencies, and bankruptcies to different groups of investors, we provide you with various offers.

Auction creates competition and ensures the best price for your Equipment Finance Accounts

The Debexpert team will be with you throughout the entire sales process to secure the highest price that works for you.

FAQ

Frequently Asked Questions: Selling equipment finance portfolios

Have a different question? Contact us or browse the full FAQ.

Other Debt Types You Can Sell on Debexpert

Equipment finance is one of many asset classes on the platform. If you hold other types of debt portfolios, Debexpert's buyer network covers them all — on the same platform, with the same process.

$1.0Bauctioned

$1.0Bauctioned $648Mauctioned

$648Mauctioned $509Mauctioned

$509Mauctioned $229Mauctioned

$229Mauctioned.avif&w=960&q=70) $208Mauctioned

$208Mauctioned $156Mauctioned

$156Mauctioned $16Mauctioned

$16Mauctioned $10Mauctioned

$10Mauctioned $3Mauctioned

$3MauctionedEquipment Finance

What to Read Next

- What Is Equipment Finance?

- What Is an Equipment Finance Agreement (EFA)?

- Equipment Leasing: A Comprehensive Guide

- Equipment Finance Brokers

- Tax Benefits of Leasing Equipment

- Best Equipment Financing Options of 2024

- Gym Equipment Finance

- DJ Equipment Financing

- Financing Music Equipment

- Farm Equipment Loans

- Construction & Heavy Equipment Financing

- Restaurant Equipment Financing

Success Stories

Past reviews from our clients

“Very happy to work together with Debexpert group specially Henry with excellent clients service and they teamwork is very professional, helpful and knowledgeable they goes the extra mile to close for any of the clients. I really admire his work ethics. He is very hardworking and always has answer to our questions. Best part he's always available to help. I would highly recommend they services. Thank you”

SKSunny Kumar

Managing Director, AAA Lenders, Inc.

“Wonderful communication and support. I have always had all of my questions answered quickly, and everyone has been accommodating to make the process as easy as possible. I always look forward to seeing the new offerings, and am excited to be building a relationship with a great company!”

PFPeter Faris

Owner, Faris Holdings, LLC

“Professional, fair, and goes the extra mile to close note purchases—especially important when dealing with unrealistic/difficult sellers.”

LNLarry Nein

Owner, Preferred Note Investors

“Henry is the Business Development rep assigned to our small boutique real estate investment firm. Henry is great with follow-up and answering any and all questions I have. We have been very pleased with both your platform and Henry's service and 'can do' approach.”

ACAl Curiel

President, Associates In Real Estate Holdings, Ltd.

“Our rep at debexpert.com has always been very proactively communicative, reaching out to make sure we are aware of trades that fit our buying box and easily accessible to answer questions and help facilitate the process.”

LLLisa Lemire

Managing Member, Kamini Bay Asset Management, LLC

Get Started

Get a Free Valuation for Your Equipment Finance Portfolio

Tell us about your portfolio and your dedicated account manager will respond within one business day with a market estimate and next steps.

Start with the seller path

Request a valuation first, or register as a buyer if you also want marketplace access.

Request a free valuation and get guided through listing your receivables.

Register as a buyer to access marketplace listings, data tapes, and auctions.