Student loan debt collection agencies recover money from borrowers who default on their loans. For federal loans, default happens after 270 days of non-payment, and these agencies use aggressive methods like wage garnishment, tax refund interception, and even seizing Social Security benefits. Private loan collectors, by contrast, require court orders for similar actions. Borrowers face added fees of up to 25% on their balances, and defaults can severely damage credit scores for years.

Here’s what you need to know:

- Federal Loan Collections: Agencies can garnish wages (up to 15%) and seize tax refunds or Social Security without a court order. Options like loan rehabilitation or consolidation can help get out of default.

- Private Loan Collections: Require court approval for wage garnishment and lack federal-level recovery tools.

- Borrower Protections: The Fair Debt Collection Practices Act (FDCPA) limits harassment and ensures borrowers can dispute debts.

- Economic Impact: Defaults affect millions, with collection actions worsening financial instability and reducing consumer spending by billions annually.

If you’re in default, act quickly to explore repayment or dispute options. Log into your Federal Student Aid account to verify loan details and avoid scams. Understanding your rights and available solutions can help you regain control of your finances.

Student loans in default to be referred to debt collection: Education Department updates

How Student Loan Debt Collection Agencies Work

Federal vs Private Student Loan Collection Powers Comparison

Federal vs Private Student Loan Collection Powers Comparison

Student loan debt collection agencies operate differently depending on whether the loans are federal or private. For federal student loans, the U.S. Department of Education partners with Private Collection Agencies (PCAs) through a competitive bidding process. These agencies are contracted to manage - not purchase - defaulted loans. When a borrower defaults, the loan is transferred from the original loan servicer to either the Department's Default Resolution Group or one of these PCAs.

Over the years, the Department has streamlined its operations, reducing the number of agencies handling new defaulters from 30 to 15. In a recent round of contracts, two agencies secured deals worth a combined $400 million. The Office of Federal Student Aid oversees these PCAs, ensuring they adhere to federal guidelines while managing the nation’s financial aid programs and defaulted loan collections.

Private student loans follow a different path. When borrowers fall behind, private lenders hire debt collectors to recover the funds. These collectors represent the lender, not the federal government, and they don’t have the same collection powers as federal agencies.

Collection Activities for Federal vs. Private Student Loans

Federal and private debt collectors have vastly different tools at their disposal. Federal agencies have more authority and don’t need court approval to take certain actions. They can:

- Garnish up to 15% of a borrower’s disposable income through administrative wage garnishment.

- Intercept federal and state tax refunds via the Treasury Offset Program.

- Withhold portions of Social Security or disability benefits.

These measures typically begin after a loan has been in default for over 360 days.

Private collectors, on the other hand, face stricter limitations. They need a court order to garnish wages and cannot intercept tax refunds or Social Security payments. As the Consumer Financial Protection Bureau explains:

"A debt collector seeking to recover a private student loan does not work for, represent, or collect on behalf of the U.S. Department of Education or any other branch of the federal government".

Defaults are also reported to major credit bureaus - Equifax, Experian, Innovis, and TransUnion - if borrowers fail to respond within 65 days of receiving a default notice. These differences in authority affect how debts are collected and the outcomes for borrowers.

| Collection Tool | Federal Student Loans | Private Student Loans |

|---|---|---|

| Wage Garnishment | Up to 15% via administrative order (no court required) | Requires a court order |

| Tax Refund Offset | Can intercept federal and state refunds | Generally not allowed |

| Social Security Seizure | Can withhold a portion of benefits | Not permitted |

| Recovery Options | Rehabilitation, Consolidation, Repayment | Must negotiate with the lender |

| Default Timeline | 270 days | Varies by contract (often sooner) |

These collection strategies highlight the stark contrast between federal and private practices and their impact on borrowers.

How Agencies Buy Student Loan Debt Portfolios

The term "buy" doesn’t accurately describe how federal student loan debt is handled. PCAs working with federal loans don’t purchase the debt; they’re contracted to manage it. The Department of Education retains ownership and compensates these agencies based on their recovery performance. Historically, the government has paid PCAs about $1,710 for each borrower who successfully completes loan rehabilitation.

This payment model creates unique dynamics. For example, while the Department spent over $700 million annually on collection services for roughly 7 million defaulted borrowers, only 4% of the recovered debt - about $354 million - came directly from payments to PCAs. The bulk of recoveries, nearly 90% of the $8.7 billion in 2016, came from federal programs like loan rehabilitation and consolidation rather than direct payments to collection agencies.

For private student loans, the process follows a more traditional debt-buying model. Lenders often sell defaulted loan portfolios to collection agencies or third-party debt buyers at a discount. These transactions are based on factors like borrower creditworthiness, loan balances, payment histories, and projected recovery rates. Specialized platforms connect sellers and buyers, ensuring compliance and facilitating the sale of student loan portfolios.

Debt Recovery Methods and Tactics

Debt collection agencies use a phased approach, starting with voluntary methods before escalating to more aggressive actions. Initial efforts include contacting borrowers through calls, letters, or emails. Before taking involuntary steps, agencies must provide notices of intent - 65 days for tax refund offsets and 30 days for wage garnishment.

Agencies often encourage borrowers to pursue loan rehabilitation, which involves making nine consecutive, on-time monthly payments. Completing this process removes the default from credit reports and returns the loan to regular servicing. However, collection fees - around 20% of each payment - are deducted before reducing the loan balance.

Consolidation is another way out of default. Borrowers can consolidate their loans into a new Direct Consolidation Loan, often paired with an income-driven repayment plan. Collection fees for this process can reach up to 18.5% of the combined principal and interest, though a flat fee of $150 is common for "forced-IDR" consolidations.

As of January 16, 2026, involuntary collection efforts like Administrative Wage Garnishment and the Treasury Offset Program are temporarily paused under the Working Families Tax Cuts Act. Nicholas Kent, Under Secretary of Education, commented:

"The Department determined that involuntary collection efforts such as Administrative Wage Garnishment and the Treasury Offset Program will function more efficiently and fairly after the Trump Administration implements significant improvements to our broken student loan system".

While PCAs handle most borrower interactions, final decisions on involuntary collections are made by federal employees at the Department of Education. The Department collaborates with the U.S. Treasury to execute offsets, but PCAs remain the main point of contact for borrowers navigating default resolution. These recovery methods have significant financial implications for borrowers and shape how student loan collections impact the broader economy.

Borrower Rights and Legal Protections

When collection agencies start contacting borrowers, it's important to know that specific legal safeguards are in place. These protections, outlined by federal law, set clear boundaries on what collectors can and cannot do - whether the debt is federal or private.

Fair Debt Collection Practices Act (FDCPA) Rights

The Fair Debt Collection Practices Act (FDCPA) applies to third-party debt collectors and creditors operating under a different name. According to the Federal Trade Commission:

"The Fair Debt Collection Practices Act (FDCPA) makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts."

Collectors must adhere to strict rules when contacting borrowers. For instance, they cannot call before 8:00 a.m. or after 9:00 p.m. local time, and they are prohibited from calling borrowers at work if explicitly told not to. The "7-7-7" rule limits calls to no more than seven times within seven days - or within seven days after a conversation about a specific debt.

Within five days of their first contact, debt collectors must send borrowers a validation notice. This notice should include the amount owed, the creditor's name, and instructions on how to dispute the debt. If a borrower disputes the debt in writing within 30 days, collection efforts must pause until the collector provides written verification. Additionally, collectors typically need to wait 14 days after sending the validation notice before reporting the debt to credit bureaus.

Borrowers can stop all contact by sending a written request - certified mail with a return receipt is recommended. After receiving this notice, collectors may only contact the borrower to confirm they will stop communication or to inform them of specific legal actions.

The FDCPA also prohibits certain behaviors, such as threats of violence, obscene language, publishing "shame lists", pretending to be attorneys or government officials, and threatening arrest for non-payment. Borrowers who experience violations can sue within one year, with potential damages of up to $1,000 for individual cases. Class action lawsuits are capped at the lesser of $500,000 or 1% of the collector's net worth. To document violations, borrowers should keep detailed records of call dates, times, and conversations. Reports can be filed with the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC). For federal student loan issues that remain unresolved, borrowers can contact the Federal Student Aid Ombudsman Group. [11, 4]

These legal protections empower borrowers to address their debts while maintaining their rights.

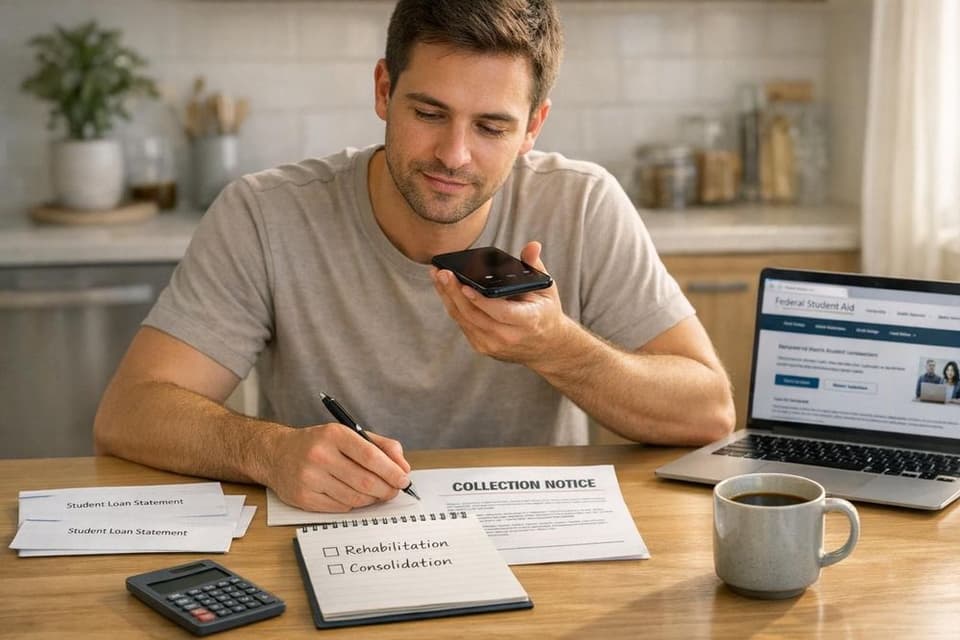

Options for Resolving Defaulted Student Loans

While the FDCPA protects borrowers from unfair practices, there are also structured ways to resolve defaulted loans. For federal student loans, borrowers can choose between rehabilitation or consolidation as recovery options.

Loan Rehabilitation requires nine consecutive on-time payments, typically amounting to 15% of discretionary income, over a 10-month period. This option is the only one that removes the default notation from credit reports entirely. Wage garnishment usually stops after the fifth payment. However, rehabilitation is generally a one-time opportunity and cannot be used again if the borrower defaults a second time. [4, 6]

Loan Consolidation involves combining defaulted loans into a new Direct Consolidation Loan with updated terms. This process takes about 4–6 weeks, during which collections cease. While the default remains on credit reports, it is marked as "paid." Unlike rehabilitation, consolidation can be used multiple times and is often paired with income-driven repayment plans. However, collection fees - up to 18.5% - may be added to the new loan balance. [4, 6, 17]

| Feature | Loan Rehabilitation | Loan Consolidation |

|---|---|---|

| Timeframe | Approximately 9 months | 4–6 weeks |

| Credit Impact | Removes default notation | Default remains (marked as "paid") |

| Availability | Generally one-time only | Can be used multiple times |

| Collection Fees | Around 20% per payment (not capitalized) | Fees may be capitalized (up to 18.5%) |

| Garnishment | Stops after the 5th payment | Stops when the new loan is disbursed |

Borrowers subject to federal administrative wage garnishment can request a hardship hearing. If other options seem unavailable, contacting the collector's Special Assistance Unit is a good next step. The CFPB advises:

"Ask to speak with the debt collector's Special Assistance Unit."

For private student loans, the process differs. These loans lack standardized federal programs for resolving defaults, so borrowers must negotiate directly with collection agencies. Options may include settling the debt or arranging a payment plan. Unlike federal loans, private loans are often governed by state-specific statutes of limitations for legal collection actions. [4, 14]

To avoid unnecessary complications, borrowers should verify all debts through the U.S. Department of Education's Federal Student Aid website. Regularly checking credit reports is also critical - remember, only rehabilitation removes the default notation for federal loans. Knowing your rights and available options can help turn financial challenges into manageable solutions.

Government Oversight and Compliance Requirements

Federal agencies play a critical role in monitoring student loan debt collection practices and enforcing consumer protection laws. The U.S. Department of Education (ED), Department of the Treasury, and Consumer Financial Protection Bureau (CFPB) share responsibility for overseeing how loans are collected and ensuring borrowers are treated fairly.

Department of Education and CFPB Regulation

The U.S. Department of Education (ED) manages the collection of defaulted federal loans, including Direct Loans and certain FFEL or Perkins loans, through its Default Resolution Group at the Office of Federal Student Aid. This ensures that federal loans under its purview are collected in compliance with established guidelines.

Meanwhile, the U.S. Department of the Treasury operates an offset program that withholds federal payments - such as tax refunds or Social Security benefits - to recover defaulted federal student loans. Borrowers are notified at least 65 days before these offsets take effect, giving them time to respond or resolve their debts.

The Consumer Financial Protection Bureau (CFPB) oversees banks, lenders, and other financial entities to ensure fair treatment of borrowers. As the CFPB explains:

"The CFPB... makes sure banks, lenders, and other financial companies treat you fairly."

The CFPB’s oversight extends to both private and federal student loan servicing and collection practices. With more than $1.7 trillion in student loan debt and roughly 28 million borrowers resuming payments after the COVID-19 pause, the CFPB has ramped up scrutiny of servicers and collectors. To guide its efforts, the agency uses an "Education loan examination" manual, which includes modules for reviewing collections, default accounts, and credit reporting. If violations are found, examiners notify companies to allow for corrections, and serious breaches may lead to formal investigations.

Regulation F (12 CFR Part 1006) sets the legal standards for enforcing the Fair Debt Collection Practices Act (FDCPA). For example, debt collectors are presumed to violate Regulation F if they call a borrower more than seven times within seven consecutive days for the same debt. The regulation also mandates clear opt-out options for email and text communications.

The Federal Student Aid Ombudsman Group, part of the ED, assists borrowers by addressing disputes with collection agencies. They also track recurring issues, such as servicing failures or program disruptions, reported by borrowers.

Borrowers can check whether their loans are held by the Department of Education by logging into their account at studentaid.gov. Loans labeled "DEPT OF ED" fall under federal oversight, while loans held by private entities are subject to different rules. For instance, private student loan collectors cannot garnish wages or intercept federal tax refunds without a court order.

Penalties for Illegal Collection Practices

Agencies that fail to comply with these regulations face serious consequences. The CFPB has the authority to issue industry bans, permanently barring companies from servicing or collecting student loans if they engage in deceptive or abusive practices.

For example, in December 2024, the CFPB penalized a debt collection agency servicing FFELP loans for delaying loan rehabilitation processes to charge additional fees. This misconduct cost borrowers thousands of dollars. The agency was banned from collecting or servicing student loans and fined $700,000, which was directed to the CFPB’s victims relief fund. Borrowers were also burdened with extra costs amounting to 16% of their loan balances. Similarly, in January 2025, the CFPB took action against the National Collegiate Student Loan Trusts for filing defective lawsuits and attempting to collect on time-barred debts. The judgment required the Trusts to pay $2.25 million in redress to borrowers and stop certain collection activities.

CFPB Director Rohit Chopra emphasized the agency's commitment to protecting borrowers:

"Companies break the law when they mislead student borrowers about their protections or deny borrowers their rightful benefits. Student loan companies should not profit by violating the law."

Enforcement measures can include financial penalties, direct compensation for borrowers, cease-and-desist orders, and restrictions on lawsuits unless claims are fully documented. For less severe violations, agencies may be required to improve their processes for addressing borrower claims. Regulators are also targeting practices like deceptive billing, unauthorized debits, and intentional delays in the loan rehabilitation process to generate extra fees.

Borrowers are encouraged to request documentation verifying that a collection agency owns their debt. This is particularly important, as some agencies have been caught suing without proper paperwork. Additionally, it is illegal for agencies to misrepresent their right to collect on "time-barred" debts - those beyond the statute of limitations. The CFPB also provides whistleblower channels for employees to report illegal practices within collection agencies.

Effects of Debt Collection on Borrowers and the Economy

Financial Consequences for Borrowers

When borrowers default on their loans, the entire balance becomes due immediately, often with collection fees as high as 25% added on top. This makes an already difficult financial situation even worse. On top of that, interest continues to build, further increasing the debt load.

Federal agencies have the authority to take extreme measures, like seizing tax refunds or garnishing wages, without needing a court order. These actions not only destabilize borrowers' finances but also severely damage their credit. Credit scores typically drop by 50 to 90 points before default, and a default record stays on credit reports for seven years. This can make it nearly impossible for borrowers to qualify for FHA or VA home loans. In some states, default can lead to the suspension of professional or driver's licenses, and for military and government personnel, it can even result in the loss of federal security clearances.

One example of the devastating effects of these measures occurred in April 2017, when a borrower’s $8,220 tax refund was seized to cover a $17,000 loan debt, leaving her family homeless.

Data shows that 84% of borrowers who default face at least one collection action, and 59% endure two or more. Wage garnishment, in particular, has a profound impact - 79% of borrowers subjected to it reported significant financial strain on their lives. Seth Frotman, the Student Loan Ombudsman at the Consumer Financial Protection Bureau, captured the severity of the issue:

"We treat struggling student loan borrowers the same as deadbeat parents and tax cheats. Even gambling addicts have more protections."

Perhaps even more alarming, over 40% of borrowers who manage to bring their loans out of default end up defaulting again within three years. These struggles don’t just affect individuals - they ripple outward, influencing the broader economy.

Economic Impact of Student Loan Collections

The financial strain on borrowers has far-reaching consequences for the economy. When student loan payments resumed in October 2023, following the end of the three-year forbearance period, consumer spending took a noticeable hit. According to Federal Reserve research, the median borrower cut their spending by roughly $130 each month. This reduction added up to an estimated $80 billion annual drop in consumer spending, equivalent to about 0.3% of the U.S. GDP and 0.4% of total personal consumption expenditures.

Beyond reduced spending, aggressive collection tactics - like wage garnishment and seizing tax refunds or Social Security benefits - further harm financially vulnerable borrowers. These measures not only worsen individual financial instability but also deepen economic inequality. As of late 2025, projections suggest that about 25% of federal student loan borrowers - around 13 million people - could be in default by the end of 2026. This default rate would surpass the 12% peak mortgage delinquency rate during the subprime mortgage crisis.

The Federal Reserve Board staff highlighted the broader implications:

"The end of forbearance amounted to a noticeable drag on aggregate demand of roughly $80 billion at an annual rate."

This reduction in spending forces many borrowers to cut back on essential needs, creating a ripple effect that slows overall economic growth.

Conclusion

Student loan debt collection agencies have unique powers that set them apart. Federal agencies, for example, can garnish up to 15% of wages, intercept tax refunds, and even seize portions of Social Security benefits - all without needing a court order. By early 2025, around 5.3 million borrowers were grappling with the challenges of managing their loans.

For borrowers, there are ways to move forward. Loan rehabilitation, which requires nine consecutive on-time payments, can remove default notations. Alternatively, loan consolidation offers quicker relief by creating a new Direct Consolidation Loan, though it still leaves a "paid" default mark on your record. However, staying out of default remains a hurdle - nearly 40% of borrowers who rehabilitate their loans end up defaulting again within three years. Acting early and consistently is essential to avoid falling back into financial trouble.

Understanding your rights under the Fair Debt Collection Practices Act is another critical step. This knowledge can shield borrowers from harassment or illegal collection tactics. Timing is also crucial: borrowers must act within 30 days of a wage garnishment notice or 65 days of an offset notice to avoid harsher penalties. These windows are narrow but offer a chance to mitigate financial damage.

The ripple effects of student loan debt go beyond individual borrowers, impacting the broader economy. This guide has explored collection methods, legal protections, and the economic consequences tied to student loan debt. Ultimately, making informed decisions is the cornerstone of navigating these challenges.

To navigate this system effectively, borrowers must verify debts through the official Federal Student Aid website, avoid paying for services the Department of Education provides for free, and choose repayment strategies that align with their long-term financial goals. Armed with the right knowledge, borrowers and stakeholders alike can take steps to minimize financial risks. Whether you're dealing with collections firsthand or involved in the recovery process, understanding how these agencies work is essential to making smarter, more informed decisions.

FAQs

How do I know if my student loan is federal or private?

To check your federal loans, log into the Federal Student Aid (FSA) website using your FSA ID. This site lists all federal loans, which are issued by the government and managed by servicers approved by the Department of Education. However, private loans - those provided by banks or other lenders - won’t show up on this platform. To determine if a loan is private, review your loan documents, check your statements, or get in touch with your loan servicer directly.

What should I do first if a collector contacts me about my student loan?

If a debt collector reaches out to you, the first step is to confirm that both the debt and the collector are legitimate. Ask for specific details, like the exact amount owed, the name of the creditor, and the collector's contact information. If they don't provide this information upfront, request that they send it to you in writing before making any payments or commitments. Taking these steps helps ensure you're addressing a valid claim and protects you from potential scams.

Which option is better for me: rehabilitation or consolidation?

Choosing between rehabilitation and consolidation comes down to your financial priorities.

Rehabilitation helps you by removing the default status from your loans, making you eligible for federal benefits again. Plus, it can improve your credit score through affordable, manageable payments. On the other hand, consolidation simplifies things by combining multiple loans into one. This can lower your monthly payments or let you switch to an income-driven plan, but it won’t erase the default status unless you first go through rehabilitation.

Think about what matters most to you - improving your credit, regaining federal benefits, or simplifying repayment - to figure out the best path forward.