A payday loan contract is a legal agreement for short-term loans, typically under $500, with very high interest rates. Borrowers repay in a lump sum, often within 45 days, using post-dated checks or bank account authorizations for automatic withdrawals. These loans are known for their strict terms and high fees, with annual percentage rates (APR) often reaching 400%. Borrowers may extend repayment for a fee, but this doesn’t reduce the principal, leading to cycles of debt.

Key points:

- Loan Amounts: Usually $500 or less.

- Repayment: Single payment due within 14–45 days; some allow extensions for a fee.

- Interest Rates: APRs can approach 400%.

- Payment Mechanisms: Lenders can withdraw funds directly from bank accounts.

- Risks: High fees, potential cycles of debt, and strict repayment terms.

State and federal regulations, like the Military Lending Act (capping APR at 36% for servicemembers) and CFPB rules, govern these loans to protect borrowers. For investors, understanding these contracts and compliance laws is critical in assessing the value and risks of payday loan portfolios.

Key Components of Payday Loan Contracts

Loan Amount and Interest Rate

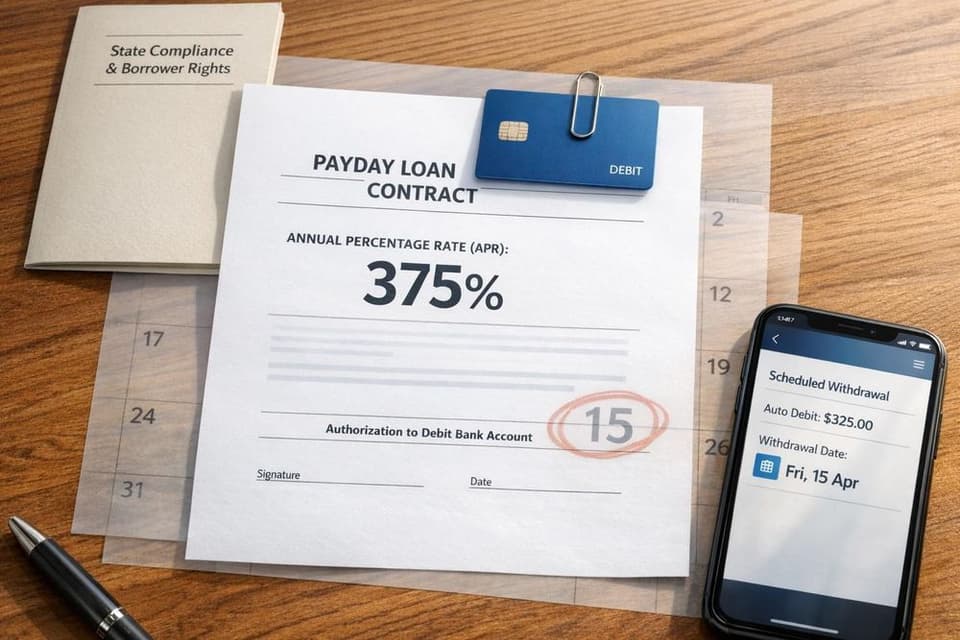

Every payday loan contract must clearly outline the Annual Percentage Rate (APR) - a crucial measure of the total annual cost of borrowing. The Consumer Financial Protection Bureau explains:

"The Annual Percentage Rate (APR) is the annual cost of credit, including fees, expressed as a percentage. The APR is a broader measure of the cost to you of borrowing money since it reflects not only the interest rate but also the fees that you have to pay to get the loan."

This federal requirement ensures borrowers understand the full financial impact of their loan. The APR accounts for not just the base interest rate but also additional charges like origination, processing, and Non-Sufficient Funds (NSF) fees, which may apply if a payment is rejected due to insufficient funds.

For alternative loans (PAL I) - which are subject to different rules - the loan amount must fall between $200 and $1,000. These loans are offered by federal credit unions, and their rates and fees must comply with federal credit union guidelines. Meanwhile, the Military Lending Act (MLA) provides protections for active-duty servicemembers and their dependents, capping the Military APR at 36%. These regulations help clarify the borrowing costs tied to payday loans and alternative options.

Repayment Terms and Schedules

The repayment terms of payday loans specify when and how borrowers are expected to repay their debt. Short-term loans typically require full repayment within 45 days of the loan agreement. Most payday loans operate on a single-payment structure, meaning the entire balance is due in one lump sum, often within 14 to 45 days.

For longer-term balloon-payment loans, repayment extends beyond 45 days, with at least one payment significantly larger than the others. In contrast, alternative loans follow a more structured schedule, requiring two or more equal payments over one to six months, with the balance fully paid off by the end of the term.

Repayment is often facilitated through ACH authorization, allowing lenders to electronically withdraw funds from the borrower's account on the due date. Borrowers do have the right to revoke this authorization, though doing so may activate default provisions. For loans with multiple payments, lenders must also provide a copy of the ACH authorization terms.

Some contracts include renewal or rollover clauses, which let borrowers pay a fee to extend the repayment deadline without reducing the principal amount. However, many states restrict or ban these clauses to prevent borrowers from falling into cycles of debt. Studies show that 80% of payday loans are renewed or rolled over within 14 days, with over 60% of these loans forming part of sequences involving seven or more loans. These repayment structures are a key factor in understanding the broader implications of payday lending.

Default and Late Payment Clauses

Default clauses detail the circumstances under which a loan is considered in default and outline the lender's rights to pursue repayment. A loan remains "outstanding" until it is fully repaid, the borrower is released from the obligation, or 180 days have passed since the last payment. The consummation clause specifies the exact point at which the borrower becomes legally bound to the loan terms.

Contracts often include NSF fees for checks or electronic payments that are returned unpaid. Under the Payday Lending Rule (12 CFR Part 1041), lenders must follow strict guidelines regarding payment transfer attempts to prevent unfair practices.

If a borrower defaults, lenders may initiate collections or legal action but generally cannot garnish wages without a court order. Importantly, borrowers cannot be arrested for failing to repay a payday loan.

| Loan Type | Repayment Period | Structure Requirements |

|---|---|---|

| Short-term Loan | Within 45 days | Typically single-payment |

| Longer-term Balloon | Over 45 days | Includes one payment larger than the others |

| Alternative Loan | 1 to 6 months | Equal installments, fully amortized |

For borrowers struggling to make payments, reviewing the loan contract or state laws can provide clarity on whether the lender must offer an extended repayment plan with smaller installments. These default provisions are essential for assessing risks, especially in the context of debt trading and portfolio management.

Legal and Regulatory Framework

Federal Regulations

The Truth in Lending Act (TILA) and Regulation Z require lenders to disclose critical loan details - like the APR and total finance charges - before a consumer is legally obligated to the agreement. Additionally, the Consumer Financial Protection Bureau's (CFPB) Payday Lending Rule (12 CFR Part 1041) sets clear boundaries for payday, vehicle title, and high-cost installment loans. Although the CFPB removed mandatory underwriting requirements in July 2020, the rule still enforces strict limits on payment withdrawal attempts. Specifically, lenders are prohibited from trying to withdraw payment after two consecutive failed attempts due to insufficient funds unless they secure new, explicit consent from the borrower. As the CFPB states:

"The rule identifies it as an unfair and abusive practice to attempt to withdraw payment from a consumer's account after two consecutive payment attempts have failed, unless the lender obtains the consumer's new and specific authorization."

Other federal laws also impose restrictions on payday lending. For example, the Military Lending Act (MLA) protects active-duty servicemembers and their families by capping the Military Annual Percentage Rate (MAPR) at 36% for most consumer loans, including payday loans. Violating the MLA can render contracts void and lead to CFPB enforcement actions.

State-Specific Rules

While federal laws provide a baseline, state regulations play a crucial role in shaping payday lending practices and contract enforceability. These rules vary widely and often determine whether a payday loan contract is valid. For example, payday loan agreements are usually enforceable only if the lender is licensed in the borrower's state. Borrowers can verify a lender's licensing status through the NMLS Consumer Access portal. Some states go further, banning payday lending outright or imposing strict usury caps, which can render certain contracts unenforceable.

Interest rate caps differ significantly across states. For instance, Montana and Oregon have a 36% cap, while states like Delaware, Idaho, and Utah impose no limits. Beyond interest rates, some states regulate fees and tie loan amounts to a percentage of the borrower's gross monthly income.

Repayment protections also vary by state. In Virginia, for example, lenders must provide a repayment plan extending over 60 days with at least four installments if a borrower defaults. Oklahoma requires a 15-day cooling-off period after a borrower takes out a third consecutive loan. Furthermore, under the Electronic Fund Transfers Act (EFTA), borrowers can revoke preauthorized auto-debits by notifying both their bank and the lender.

While federal regulations establish minimum standards, state laws can impose stricter rules. In states where payday lending is banned, contracts may be void even if they meet federal disclosure requirements. Additionally, lenders operating from tribal lands sometimes claim immunity from state interest rate caps, though this remains a contentious legal issue in many state courts. Understanding these overlapping regulatory frameworks is critical for evaluating risks and assessing portfolio values in debt trading.

Understanding the CFPB's Payday Loan Rule: Implications and Compliance

Evaluating Payday Loan Portfolios for Debt Trading

Payday Loan Statistics: Borrower Behavior and Default Rates

Payday Loan Statistics: Borrower Behavior and Default Rates

Risk Assessment and Borrower Metrics

When diving into a payday loan portfolio, the first thing to examine is loan sequences - these are subsequent loans taken shortly after the initial one. According to CFPB data, most payday loans are either rolled over or renewed within 14 days, creating extended borrowing cycles. This data is key to understanding how borrower habits influence the overall risk of a portfolio.

Borrowers who depend on monthly government benefits are particularly high-risk, with 20% remaining in debt for an entire year. On the flip side, only 15% of payday borrowers manage to repay their loans on time without taking out another loan within 14 days. It's also crucial to evaluate how payments are processed - whether through post-dated checks or authorized electronic withdrawals - as this impacts both cash flow security and the likelihood of recovering funds.

Portfolio Diversification and Concentration Risks

Beyond individual borrower behavior, the makeup of the portfolio and its geographic spread play a big role in determining risk. Geographic concentration is especially critical because state regulations vary widely. For instance, portfolios heavily concentrated in states with strict usury caps or mandatory cooling-off periods will perform differently than those in states with looser rules. Breaking down portfolios by state is essential to account for these regulatory differences when pricing them.

Borrower demographics also affect portfolio value. For example, 22% of new loans are renewed six or more times. With a typical 15% fee, these borrowers often pay more in fees than the original loan amount. While this might seem profitable at first glance, it comes with a trade-off: higher default risk. Over a year, 20% of payday borrowers default on at least one loan. Portfolios with a high percentage of long-term repeat borrowers need careful risk adjustments to reflect this heightened default probability.

Legal Compliance Review

Ensuring legal compliance is another critical step in accurately valuing a payday loan portfolio. One key factor is determining whether loans are classified as "covered loans" under 12 CFR Part 1041. This classification applies to short-term loans (repayment within 45 days), longer-term balloon-payment loans, and high-cost longer-term loans with an APR over 36% that use a leveraged payment mechanism. As the CFPB highlights:

"A loan that is not a covered loan when it is made can later become a covered loan. A loan may become a covered loan at any time during the loan's term".

It's also important to verify that the portfolio complies with the Payday Lending Rule, especially the prohibition on withdrawal attempts after two consecutive failed attempts. Additionally, check whether loans qualify for exemptions, like alternative or accommodation loans. Non-compliance can lead to CFPB enforcement actions, which could severely reduce the portfolio's value through legal penalties and restrictions on collections.

Common Pitfalls and Best Practices in Payday Loan Contracts

Problematic Clauses to Watch For

When it comes to payday loan contracts, certain clauses can create serious challenges for borrowers. One major concern is leveraged payment mechanisms. These clauses allow lenders to pull payments directly from your bank account using methods like ACH transfers, remotely created checks, or account set-offs. Unlike "push" payments - where you control the timing and amount - these "pull" mechanisms put the lender in control.

Another red flag is delinquency-triggered recurring debit authorizations. These clauses can lead to repeated withdrawal attempts after a missed payment, trapping borrowers in a cycle of fees and overdrafts. Balloon payment structures, which require a large final payment far exceeding earlier installments, may also bring additional federal requirements into play.

Rollover and renewal clauses are equally concerning. These clauses allow lenders to extend loans instead of requiring repayment, often tacking on new fees with each extension. For longer-term loans, if the annual percentage rate (APR) exceeds 36% and uses a leveraged payment mechanism, the loan may fall under strict federal "Covered Loan" rules. Additionally, some contracts reference wage garnishment in ways that can be misleading, as garnishment generally requires a court order.

Spotting these issues emphasizes the importance of carefully reviewing payday loan contracts before signing.

Best Practices for Contract Drafting and Review

To address these issues, contracts should be designed to protect both borrowers and lenders while maintaining compliance with legal standards. Start by clearly distinguishing between payment types - borrowers need to understand whether they’re authorizing lender-initiated "pull" transactions or borrower-initiated "push" transactions. For loans seeking exemptions from certain regulations, alternative loans should have a principal amount between $200 and $1,000 and must include structured, equal, and fully amortizing payments.

State licensing is another critical factor. Lenders must be licensed in the borrower’s state before finalizing any contract. For loans involving active-duty servicemembers, contracts should comply with the Military Lending Act (MLA), which includes special protections like rate caps. Additionally, lenders should verify recurring income documentation for alternative loans and ensure APR disclosures are clear and upfront, rather than relying solely on flat fees.

It’s also worth noting that lenders making fewer than 2,500 covered loans annually and deriving less than 10% of their receipts from such loans may qualify for certain exemptions. However, these exemptions require meticulous documentation and ongoing compliance monitoring.

Conclusion

Payday loan contracts play a central role in defining the obligations between lenders and borrowers. They also influence the value and enforceability of debt portfolios in the trading market. These agreements outline crucial details - like repayment terms, APR disclosures, and payment mechanisms - that affect everyone involved. For lenders, well-structured contracts ensure compliance with laws such as 12 CFR Part 1041 and the Military Lending Act. For borrowers, understanding these terms can help prevent scenarios where fees outweigh the original loan amount.

The numbers paint a striking picture of payday loan realities. Around 80% of payday loans are renewed within two weeks, and in 60% of cases, borrowers end up paying fees that exceed the original loan principal. Additionally, 20% of payday borrowers default on their loans at least once during the year. These figures underscore the importance of clear, compliant contract terms to support both legal obligations and better financial outcomes.

For investors, contract compliance is a critical factor. Those investing in debt portfolios must ensure that loans were issued fairly, with proper state licensing, and in adherence to the Military Lending Act’s 36% APR cap for servicemembers. A single non-compliant contract involving an active-duty servicemember could render the associated debt unenforceable, posing significant risks.

As regulations continue to evolve - focusing on ability-to-repay standards and limiting repeated payment transfer attempts after insufficient funds - understanding the finer details of payday loan contracts becomes even more important. Well-drafted agreements not only make borrowing more manageable but also help prevent borrowers from falling into unmanageable cycles of debt.

FAQs

Can I cancel a payday loan after signing?

Yes, it’s possible to cancel a payday loan after signing, but there’s typically a very short window to act - often by the next business day. To cancel, you’ll need to notify the lender in writing and return any funds you’ve received or uncashed checks. Keep in mind, the exact process and timeframe can vary depending on your state’s laws, so it’s a good idea to review your local regulations for specific details.

What makes a payday loan contract unenforceable?

A payday loan contract becomes invalid if it includes terms that break federal or state laws. For instance, clauses like hold-harmless agreements, confessions of judgment, or waivers of consumer rights are not allowed under regulations set by agencies like the CFPB. These provisions violate consumer protections, making the contract unenforceable in the eyes of the law.

How do investors price payday loan portfolios?

Investors assess the value of payday loan portfolios by diving into aspects like loan volume, default rates, and borrower risk profiles. Several factors play a role in this evaluation, including pricing strategies, regulatory limitations, and borrower habits - particularly income instability and the tendency for repeat borrowing.

Interestingly, profitability in this space isn't just about setting high interest rates. Instead, it hinges on effectively managing defaults and ensuring solid loan performance. The ultimate aim? To strike the right balance between generating returns and keeping default-related expenses under control.