New York has some of the strictest debt collection laws in the U.S., combining federal, state, and local regulations to protect consumers. Key points include:

- Shortened Statute of Limitations: The Consumer Credit Fairness Act reduced the time to file lawsuits for consumer credit debts from 6 years to 3 years. Payments or acknowledgments no longer reset this timeline.

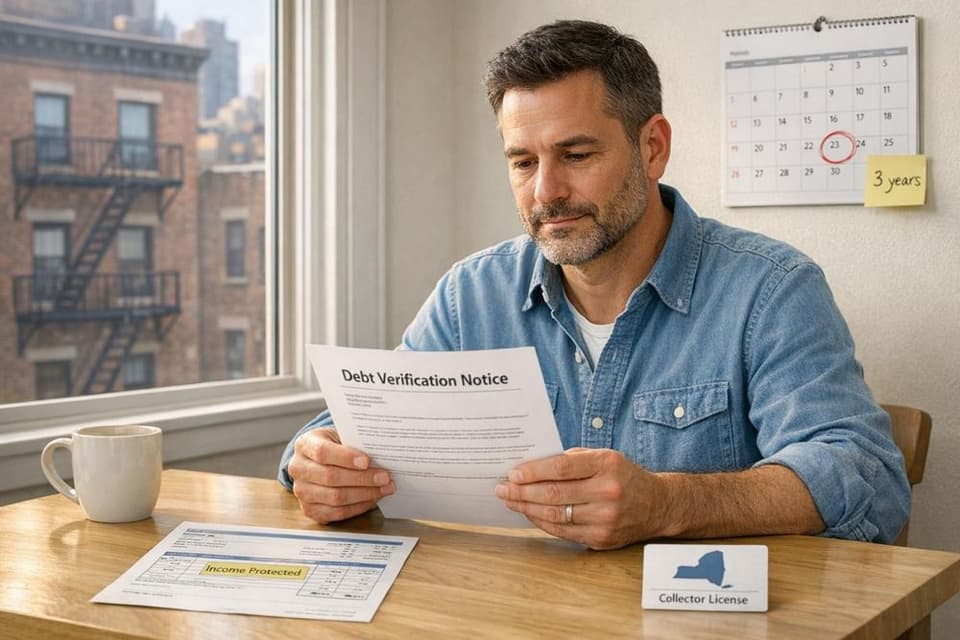

- Time-Barred Debt Rules: Collectors cannot sue or threaten legal action for debts beyond the statute of limitations. They must notify buyers when selling expired debts.

- Licensing Requirements: Debt collectors need a license to operate in New York City, including out-of-state agencies collecting from NYC residents.

- Coerced Debt Protections: Starting March 19, 2026, debts tied to economic abuse will face stricter verification rules, halting collection if claims are filed.

- Income Protections: Certain wages and funds (e.g., Social Security, unemployment benefits) are exempt from collection.

- Mandatory Disclosures: Collectors must provide detailed debt breakdowns and notify consumers of their rights, including proof of debt upon request.

Compliance is critical, as violations can lead to severe penalties. Collectors must maintain complete documentation, verify debts, and follow disclosure rules to avoid legal and financial consequences.

Ultimate Guide to Debt Collection Law in New York

Primary Regulations Governing Debt Collection in New York

New York Debt Collection Statute of Limitations by Debt Type

New York Debt Collection Statute of Limitations by Debt Type

New York's debt collection rules are shaped by a mix of laws designed to protect consumers and ensure ethical practices among debt buyers and collectors. For those in the business of buying or selling debt, understanding these regulations is critical to staying compliant and avoiding costly penalties.

Time Limits for Collecting Debt

The Consumer Credit Fairness Act has significantly shortened the statute of limitations for consumer credit transactions, such as credit card debt, to just three years from the date of default. This is a sharp reduction from the previous six years and applies retroactively to all relevant transactions. Other types of debt, however, have different timelines: written contracts generally have a six-year limit, rent overcharge claims are capped at four years, real property and mortgage actions can be pursued for up to 10 years, and alimony or child support claims extend to 20 years. These varying deadlines mean debt buyers must carefully assess the risks associated with different types of debt.

"The law changes the statute of limitations on lawsuits filed by creditors from six years to three years. Also, making payments on the debt does not restart the statute of limitations." – New York City Bar

One key consumer protection is that, as of April 7, 2022, voluntary payments or acknowledgments of consumer credit debt no longer restart the statute of limitations clock. Debt collectors are also barred from initiating or threatening legal action on time-barred debts. When selling these debts, sellers must clearly inform buyers that the statute of limitations has expired. These measures highlight New York's focus on shielding consumers from outdated or unfair collection practices.

Coerced Debt Protections Under Article 29-HHH

Starting March 19, 2026, Article 29-HHH will address debts tied to economic abuse or coercion. While the full details of this regulation are still emerging, debt buyers should anticipate stricter verification requirements and potential challenges to the validity of certain debts. This reflects New York's broader effort to address less conventional debt collection scenarios and expand consumer protections.

Licensing Rules for Debt Collectors

Beyond time limits, New York requires debt collectors to meet strict licensing standards. Unlike some states, New York regulates debt collector licensing at the local level. For example, in New York City, any business primarily engaged in collecting personal or household debts must obtain a Debt Collection Agency license from the Department of Consumer and Worker Protection (DCWP). This applies to debt buyers collecting directly or through third parties, regardless of where the business is based. Even out-of-state agencies must secure a license if they collect from NYC residents. Attorneys and law firms involved in debt collection also fall under this requirement.

Here’s the fee schedule for NYC Debt Collection Agency licenses, based on the filing period:

| License Filing Period | Fee (2-year period) |

|---|---|

| February 1 – July 31 (odd year) | $150 |

| August 1 (odd year) – January 31 (even year) | $113 |

| February 1 – July 31 (even year) | $75 |

| August 1 (even year) – January 31 (odd year) | $38 or $188 |

NYC licenses expire every two years on January 31 of odd-numbered years. Agencies handling child support payment debts must also post a $5,000 surety bond. Additionally, credit card payments for licenses include a nonrefundable 2% convenience fee.

New York also enforces 23 NYCRR 1, which imposes strict requirements for substantiating debt claims. If substantiation lapses when a debt portfolio changes hands, the new buyer must renew the verification process to ensure the debt is valid. For charged-off debts, new buyers are required to provide initial disclosures and offer substantiation, even if a previous collector already did so. Collectors who are subject to both DCWP and Department of Financial Services rules can streamline compliance by issuing a single disclosure that satisfies both sets of requirements.

Consumer Protections in New York Debt Collection

New York has put in place a strong set of rules to shield consumers from aggressive debt collection tactics. Some protections are automatic, while others require individuals to take specific actions. These measures work alongside broader regulations to ensure consumers are informed and safeguarded.

Income and Assets Protected from Collection

The Exempt Income Protection Act (EIPA) ensures that certain funds in bank accounts, payment apps, and prepaid cards are off-limits to debt collectors. For instance, banks cannot freeze or seize a minimum amount from a consumer's account. In 2026, this baseline protection is set at $4,080 for residents of New York City, Long Island, and Westchester, and $3,840 for those in other parts of the state.

Wages are also well-protected. Under New York law, 90% of wages or salary earned in the last 60 days cannot be collected. Additionally, as of January 2025, wages below $495 per week after taxes are completely protected. Government benefits, pensions, and certain retirement funds are also safeguarded. However, if a bank freezes funds beyond the automatic limit, consumers may need to file an exemption claim within 20 days.

"If a creditor or debt collector receives a money judgment against you in court, state and federal laws may prevent the following types of income from being taken to pay the debt: 1. Supplemental security income (SSI); 2. Social security; 3. Public assistance (welfare); 4. Spousal support, maintenance (alimony) or child support; 5. Unemployment benefits; 6. Disability benefits; 7. Workers' compensation benefits; 8. Public or private pensions; 9. Veterans' benefits; 10. Federal student loans, federal student grants, and federal work study funds; and 11. Ninety percent of your wages or salary earned in the last sixty days." – N.Y. Comp. Codes R. & Regs. Tit. 23 § 1.2

However, these protections generally do not extend to debts related to taxes, child support, spousal support, or federal student loans.

Required Disclosures and Communication Rules

Beyond licensing rules and time limits, New York mandates that debt collectors provide clear disclosures to protect consumers. Within five days of first contact, collectors must send a written notice that explains consumer rights under the Fair Debt Collection Practices Act (FDCPA). This includes bans on harassment, obscene language, and threats, as well as a list of income types exempt from collection. For charged-off debts, the notice must also include the original creditor's name and an itemized breakdown of the debt.

For time-barred debts, collectors are required to notify consumers before accepting any payment:

"Your creditor or debt collector believes that the legal time limit (statute of limitations) for suing you to collect this debt may have expired... if you make a payment on the debt, admit to owing the debt, promise to pay the debt, or waive the statute of limitations on the debt, the time period in which the debt is enforceable in court may start again." – N.Y. Comp. Codes R. & Regs. Tit. 23 § 1.3

Consumers also have the right to demand proof of the debt. If such a request is made, all collection efforts must stop until documentation is provided - typically within 60 days. For payment plans, collectors must send quarterly updates detailing how payments are applied, interest accrued, and the remaining balance. Once a debt is fully paid, written confirmation must be issued within 20 days.

These rules apply to all debt collectors operating in New York, emphasizing the state's dedication to protecting consumers and ensuring fair debt collection practices.

How to Ensure Compliance When Trading Debt Portfolios

Trading debt portfolios in New York is no simple task. It requires thorough documentation, adherence to strict legal timelines, and a commitment to protecting consumer rights. Skipping essential verification steps can lead to unenforceable debt purchases and hefty penalties. New York law demands complete records and swift responses to consumer claims, making attention to detail critical.

Verifying Debt Portfolio Accuracy

Before any transaction, it's essential to confirm that each account in the portfolio has an unbroken chain of title, tracing ownership from the original creditor to the current owner. Missing links here mean you may lack the legal standing to pursue claims in New York courts. Additionally, ensure that consumer credit debts are still within enforceable time limits - debts that have aged beyond this are often referred to as "zombie debt" and cannot legally be collected.

To meet New York's heightened legal requirements, portfolios must include:

- The original contract or charge-off statement.

- An itemized account summary detailing the charge-off amount, accrued interest, fees, and payment history.

Without these records, you won't be able to meet the 60-day substantiation deadline for consumer proof requests. Consumer rights attorney Adam Wolf emphasizes this point:

"Incomplete records are no excuse to pursue questionable suits. The onus remains on collectors to substantiate their allegations, not force defendants to disprove false claims".

| Required Information for Debt Verification | Legal Source |

|---|---|

| Identity of the original creditor | 23 NYCRR 1 / CCFA |

| Unbroken chain of assignments (Chain of Title) | CCFA / CPLR 3016(j) |

| Itemized breakdown (principal, interest, fees, payments) | 23 NYCRR 1.2(b) |

| Original contract or charge-off statement | CCFA / CPLR 3016(j) |

| Statute of limitations status (3-year lookback) | CCFA |

In addition to verifying documentation, traders must be prepared to address unique issues like coerced debt claims.

Managing Coerced Debt Claims

Starting March 19, 2026, New York's Article 29-HHH will introduce new rules around coerced debt. This type of debt includes obligations incurred through economic abuse, fraud, intimidation, or the unauthorized use of personal information. If a debtor submits a sworn statement with supporting documents (like police or FTC reports), all collection activities must stop immediately.

Key steps include:

- Notifying consumer reporting agencies within 10 business days.

- Completing a full review of the claim within 30 days.

- Avoiding contact with the alleged abuser or sharing the debtor's documentation without their written consent.

Joseph D. Simon, a partner at Cullen and Dykman LLP, advises:

"Financial institutions and other lenders operating in New York should review their procedures to address coerced debt claims, including establishing channels to receive a debtor's sworn statement and adequate documentation, pausing collection upon receipt, notifying consumer reporting agencies, and completing a documented review within the statutory timelines".

Violations can result in $1,000 in statutory damages per incident, plus actual damages and attorney fees. The New York Attorney General can also impose civil penalties of up to $5,000 per violation. To avoid transferring compliance risks, sellers should thoroughly screen portfolios for active coerced debt claims before listing them.

Using Debexpert to Maintain Compliance

Debexpert

Debexpert offers tools to simplify compliance with New York's stringent requirements. The platform streamlines the documentation review and verification process, ensuring all necessary records are in place before transactions proceed. Sellers can securely upload original contracts, charge-off statements, and itemized account summaries using Debexpert's secure file sharing system, which features end-to-end encryption to protect sensitive data.

Debexpert also provides portfolio analytics tools to help identify accounts nearing the three-year statute of limitations or those with missing documentation that could hinder compliance with the 60-day substantiation rule. The real-time chat feature allows buyers and sellers to resolve questions about coerced debt claims, licensing, or incomplete records before finalizing a sale.

For portfolios involving New York City accounts, sellers can confirm that buyers hold the required DCWP Debt Collection Agency license ($150 for a two-year term). The platform’s auction setup features - offering English, Dutch, Sealed-bid, and Hybrid formats - come with built-in compliance checkpoints to ensure smooth transactions. Notifications also alert buyers when portfolios matching their licensing and operational criteria become available, adding an extra layer of convenience to the process.

Summary: Navigating New York Debt Collection Laws

Debt collection in New York demands accuracy and diligence, especially for debt portfolio traders. The Consumer Credit Fairness Act has reduced the statute of limitations for consumer credit transactions from six years to three. Importantly, this timeline cannot be reset by debtor payments or acknowledgments. As a result, portfolios must be carefully reviewed for age, as time-barred debts come with strict disclosure requirements and limited collection options.

The documentation process is equally rigorous. Collectors must provide a clear chain of title, tracing ownership of the debt from the original creditor to the current holder. Each transfer must be supported by affidavits. Without the original contract or charge-off statement, meeting the 60-day deadline to substantiate a debt upon consumer request becomes unfeasible. The shortened statute of limitations further emphasizes the importance of maintaining complete and accurate records, as no additional time is granted even if the debtor acknowledges or partially pays the debt.

Consumer protection measures play a key role in reinforcing these standards. Collectors are required to present an itemized accounting of the debt, detailing the balance at charge-off along with all subsequent interest, fees, and payments. Furthermore, detailed reporting obligations are mandatory throughout the collection process. These are not optional guidelines but strict regulatory requirements, with penalties for failing to comply.

FAQs

How do I know if my debt is time-barred in New York?

In New York, figuring out if your debt is time-barred involves a few key steps. First, identify the type of debt you’re dealing with, as the statute of limitations varies. For example, some debts have a limit of 3 years, while certain judgments can stretch up to 20 years.

Next, pinpoint when the clock started ticking on the limitations period. This usually begins from the date of your last payment. However, be careful: if you make a payment or even acknowledge the debt, it might reset the clock, giving creditors more time to take legal action.

If the statute of limitations has expired, you can use it as a defense against lawsuits. However, keep in mind that while creditors may no longer sue you, they can still attempt to collect the debt through other legal means.

What proof can I request from a debt collector in New York?

In New York, you have the right to request a written validation of a debt from a collector. This document should clearly outline details such as the amount owed, the name of the creditor, and whether the debt is considered time-barred under state laws. Ensuring the information is both detailed and accurate is essential for meeting legal requirements.

Do debt collectors need a license to collect in New York City?

Debt collectors are required to hold a Debt Collection Agency License to operate in New York City. This license is issued by the NYC Department of Consumer and Worker Protection (DCWP).