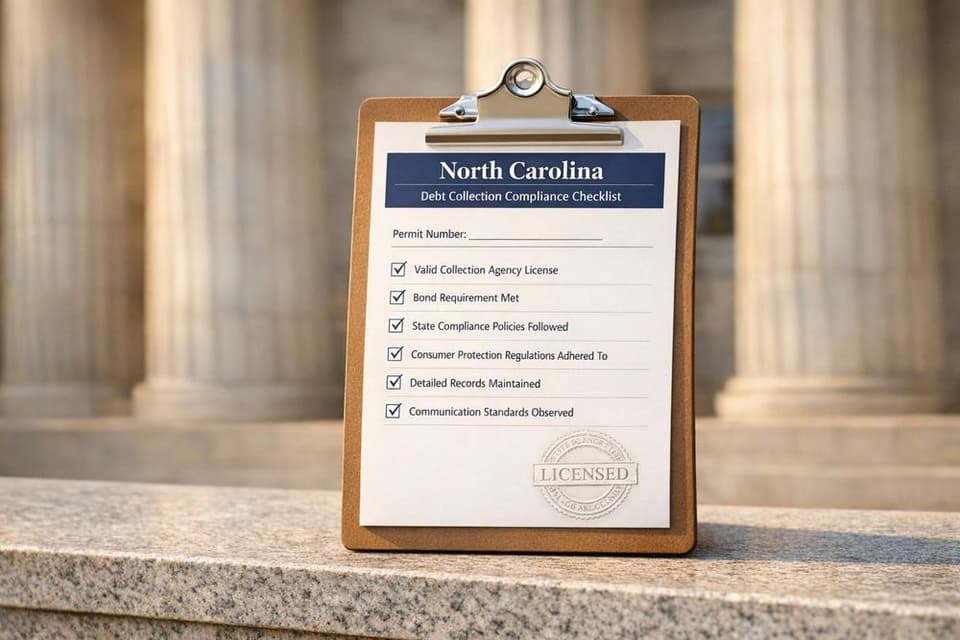

Debt collection in North Carolina is tightly regulated to protect consumers and ensure ethical practices. Here’s what you need to know:

- Licensing: All collection agencies must be licensed by the North Carolina Department of Insurance. Operating without a license is a Class I felony.

- Permit Number Requirement: Starting July 1, 2024, agencies must include their North Carolina Permit Number on all correspondence.

- Consumer Protections: State laws prohibit wage garnishment for family support (last 60 days) and require a 30-day notice before lawsuits.

- Statute of Limitations: Most debts (e.g., credit cards, medical bills) have a 3-year limit, while mortgages and sealed contracts last up to 10 years.

- Federal and State Laws: The Fair Debt Collection Practices Act (FDCPA) and North Carolina Debt Collection Act (NCDCA) set strict guidelines for communication and debt recovery.

For agencies, compliance with these rules is non-negotiable. Violations can result in severe penalties, including fines, lawsuits, and license suspension. Collecting ethically and following legal requirements isn’t just about avoiding penalties - it builds trust and improves recovery rates.

Debt collection complaints spike in the Carolinas

North Carolina Licensing and Legal Requirements

North Carolina Debt Collection Agency Licensing Requirements by Location

North Carolina Debt Collection Agency Licensing Requirements by Location

These rules and regulations play a key role in maintaining ethical standards within North Carolina's debt collection industry.

North Carolina Collection Agency Act (NCCAA) Overview

North Carolina Collection Agency Act

The North Carolina Collection Agency Act (NCCAA), found in NCGS Chapter 58/Article 70, provides the legal foundation for all collection agency operations within the state. Any business involved in debt collection, including debt buyers who acquire delinquent accounts, must obtain a permit from the North Carolina Department of Insurance (NCDOI). Applications are managed through the North Carolina License Management System (NCLMS) and include a two-step review process: an initial evaluation by PearsonVUE, followed by a regulatory review by the NCDOI. The entire process typically takes 4 to 8 weeks. Applicants need to pay a $1,000 fee and secure a surety bond. Bond amounts differ based on the agency's location: $10,000 for resident agencies, $20,000 for nonresident agencies, and $40,000 for agencies outside the U.S. Licenses must be renewed annually by June 30, with bond adjustments reflecting the previous year's collections (usually between $10,000 and $30,000, calculated as one-sixth of total collections minus commissions). Agencies are encouraged to submit renewal applications at least 30 days before the deadline to avoid penalties or license denial.

Starting July 1, 2024, all licensed agencies must include their NC Permit Number on correspondence, and each branch must secure its own license.

Additional operational and reporting requirements are also part of the licensing process, as detailed below.

| Requirement | Resident Agency | Nonresident Agency | Alien Agency (Outside U.S.) |

|---|---|---|---|

| Initial Permit Fee | $1,000 | $1,000 | $1,000 |

| Initial Bond Amount | $10,000 | $20,000 | $40,000 |

| Trust Account | NC-based or Commissioner-approved | Separate account for NC creditors | Same as Nonresident |

| Permit Expiration | June 30 | June 30 | June 30 |

State Compliance Requirements

Once licensed, agencies must meet stringent operational standards. All funds collected must be deposited into a trust account within two banking days of receipt. Agencies working with North Carolina-based clients are required to maintain a separate trust account specifically for those clients. Agencies that only negotiate payment arrangements may apply for an exemption from maintaining a trust account through an official attestation with the NCDOI. Additionally, any new or updated correspondence, forms, or brochures must be submitted to the Commissioner for approval prior to use.

When accepting cash payments, agencies must issue prenumbered receipts that include the permit number, creditor name, payment amount, date, and the payer's last name. These receipts must be retained for three years.

The NCCAA also outlines prohibited practices to ensure fairness. Agencies cannot collect unauthorized fees or interest, seek affirmations of debt from consumers in bankruptcy without proper disclosure, or contact debtors who are represented by an attorney. Debt buyers are required to send a 30-day written notice before initiating legal action and must have documentation proving ownership of the debt, along with an itemized breakdown of the owed amount.

Collection agencies and their representatives are explicitly barred from practicing law. This includes appearing in small claims court on behalf of creditors unless they are licensed attorneys. Agencies must also report specific changes promptly: address or email updates within 10 business days, criminal convictions involving dishonesty or breach of trust within 10 days, and administrative actions from other states within 30 days. If there is a change in ownership of 50% or more, the agency must apply for a new license and obtain a new permit number.

Federal and State Consumer Protection Laws

In North Carolina, both federal and state laws work together to regulate how debt collectors operate, setting clear rules for communication and debt recovery while protecting consumers. These laws form a strong foundation for ethical debt collection practices in the state.

Fair Debt Collection Practices Act (FDCPA)

The FDCPA establishes nationwide rules for debt collection. Collectors can only contact consumers between 8 a.m. and 9 p.m. local time and are not allowed to call workplaces if it's prohibited. Within five days of the first contact, collectors must send a written notice detailing the debt amount, the creditor's name, and the consumer's right to dispute the debt within 30 days.

The law strictly forbids harassment, threats, profanity, and excessive calls. Collectors also cannot falsely claim to represent attorneys or government officials, misrepresent the debt amount, or threaten legal action they don't plan to take. If a consumer sends a written request to stop communication, the collector must comply, except to inform the consumer about legal remedies or the end of collection efforts.

If collectors violate these rules, consumers can sue for actual damages plus up to $1,000 in additional damages. In class action cases, the total recovery is capped at the lesser of $500,000 or 1% of the collector's net worth. While the FDCPA sets the federal standard, North Carolina's laws go even further.

North Carolina Debt Collection Act (NCDCA)

The NCDCA expands on federal protections and applies to anyone involved in debt collection, including original creditors like landlords and homeowners associations. It also covers attorneys collecting debts for clients, regardless of how often they do so.

"Unlike the federal Act, the NCDCA does not limit its definition to those collecting debts on behalf of others, and thus, a homeowners association attempting to collect assessments owed to it or a landlord seeking to recover past-due rent and related charges are debt collectors within the meaning of the statute."

The NCDCA prohibits five main types of misconduct: threats and coercion, harassment, unreasonable publication, deceptive representation, and unconscionable practices. For debt buyers, it is illegal to sue or initiate arbitration if they know - or should reasonably know - that the debt is time-barred under the statute of limitations.

State law allows consumers to claim statutory damages ranging from $500 to $4,000 per violation, compared to the federal maximum of $1,000. Operating a collection agency without a state permit is considered a Class I felony, and knowingly participating in other violations can result in a Class 1 misdemeanor. Additionally, the Commissioner of Insurance has the authority to seek restraining orders, injunctions, and suspend permits automatically after a conviction.

The table below highlights the differences between the FDCPA and North Carolina's regulations:

| Provision | FDCPA Requirement | NC State Specifics (NCDCA/NCCAA) |

|---|---|---|

| Call Times | 8 a.m. – 9 p.m. | Same as federal |

| Statutory Damages | Up to $1,000 | $500 to $4,000 per violation |

| Applies to Original Creditors | Generally No | Yes (e.g., Landlords, HOAs) |

| Attorney Coverage | Only if they "regularly" collect | All attorneys collecting debt |

| Debt Validation | 5-day notice required | Itemized accounting and original creditor info |

Statute of Limitations for Debt in North Carolina

Knowing the time limits for debt collection in North Carolina is crucial for navigating the state's legal system. These deadlines determine how long creditors or collectors have to file a lawsuit to recover unpaid debts. Once the statute of limitations expires, the debt becomes "time-barred", meaning collectors can no longer sue for repayment - though the debt itself doesn’t disappear.

Debt Types and Time Limits

North Carolina’s laws set specific timeframes for different types of debt, which influence how creditors approach collection. For instance, credit card debt and medical bills generally fall under a 3-year statute of limitations, starting from when the debtor misses a payment. Personal loans and oral contracts also share this 3-year limit.

On the other hand, auto loans and contracts involving the sale of goods have a 4-year limitation period, while mortgages and contracts signed under seal are enforceable for up to 10 years. Additionally, if a creditor secures a court judgment, that judgment remains valid for 10 years.

| Debt Type | Statute of Limitations | Legal Reference |

|---|---|---|

| Credit Card Debt | 3 Years | N.C. Gen. Stat. § 1-52 |

| Medical Debt | 3 Years | N.C. Gen. Stat. § 1-52 |

| Personal Loans / Promissory Notes | 3 Years | N.C. Gen. Stat. § 1-52 |

| Oral / Spoken Contracts | 3 Years | N.C. Gen. Stat. § 1-52 |

| Auto Loans (Contracts of Sale) | 4 Years | N.C. Gen. Stat. § 25-2-725 |

| Mortgages | 10 Years | N.C. Gen. Stat. § 1-47 |

| Contracts Signed Under Seal | 10 Years | N.C. Gen. Stat. § 1-47 |

| Court Judgments | 10 Years | N.C. Gen. Stat. § 1-47 |

These varying timeframes mean that creditors must adjust their collection strategies based on the type of debt and its corresponding deadline.

Impact on Collection Efforts

Once a debt becomes time-barred, collectors lose the ability to file lawsuits or initiate arbitration. However, they can still attempt to recover the amount through communication, such as letters or phone calls, as long as they comply with strict regulations. Any violation of these rules can lead to penalties, with statutory damages ranging from $500 to $4,000 per infraction.

Agencies seeking a debtor’s written acknowledgment of a time-barred debt must be transparent. They are required to inform the consumer that they are not legally obligated to confirm the debt and must explain the potential consequences of doing so.

It’s also essential for both creditors and debtors to keep accurate records. For creditors, maintaining receipts and transaction histories for at least 3 years helps track delinquency dates and statute limits. Debtors should be cautious, as even a small payment or written acknowledgment can reset the statute of limitations, allowing creditors to pursue legal action once again.

Best Practices for Debt Collection Agencies in North Carolina

Communication Standards and Ethics

Debt collectors in North Carolina must adhere to specific rules when contacting consumers. They are only allowed to reach out between 8:00 a.m. and 9:00 p.m. local time, unless the debtor has explicitly agreed to a different schedule. During the first contact, collectors must clearly state the purpose of the communication and explain how the information will be used.

Transparency is a key requirement. Agencies must use their real business name, display their North Carolina permit number on all communications, and avoid any form of deception, such as using false identities or misrepresenting their affiliations. When reaching out to third parties, like neighbors or relatives, collectors are restricted to only asking for location information. Discussing the debt itself with third parties is strictly prohibited.

"No collection agency shall collect or attempt to collect any debt alleged to be due and owing from a consumer by means of any unfair threat, coercion, or attempt to coerce." – North Carolina General Statute § 58-70-95

If a debtor submits a written request to stop communication or notifies the agency about restrictions on workplace calls, collectors must comply and cease further contact, except for legally mandated notices. Harassment, such as using profane language, threats of violence, or making repeated calls intended to annoy, is strictly forbidden. Violations can lead to penalties ranging from $500 to $4,000 per incident.

Additionally, agencies must seek approval from the Commissioner of Insurance before using any new letters, forms, or brochures. By following these ethical communication standards, agencies can establish trust and maintain compliance, which is crucial for effective debt collection.

Improving Collection Recovery Rates

To improve recovery rates, agencies must prioritize accurate data management and meticulous recordkeeping. Debt buyers are required to verify all debt details, including original account numbers, and maintain complete records as mandated by state law. North Carolina regulations require agencies to keep detailed records of every business transaction conducted in the state. These records, including evidence of all receipts, must be preserved for at least three years. When accepting cash payments, agencies should provide prenumbered receipts that include critical details like the agency’s permit number, the creditor's name, the payment amount, and the remaining balance.

Collected funds must be deposited into a trust account within two business days to ensure proper handling.

Agencies must also avoid engaging in activities that could be considered the unauthorized practice of law. For example, representatives who are not licensed attorneys cannot prepare legal documents, such as warrants or subpoenas, nor can they appear in small claims court on behalf of a creditor. If legal action is necessary, agencies should collaborate with a licensed attorney. Furthermore, once a debtor is represented by legal counsel, all communication must go through the attorney.

Compliance isn’t just about avoiding fines - it’s about fostering trust and creating a sustainable operation. Agencies that respect consumer rights, provide clear debt validation within five days of initial contact, and honor cease communication requests tend to see more positive outcomes. When consumers see that an agency is operating within the law and treating them fairly, they are more likely to engage in productive negotiations, reducing disputes and improving recovery rates.

Debt Portfolio Trading in North Carolina

Navigating North Carolina’s strict regulations can be challenging for agencies involved in debt portfolio trading. However, using technology can make the process more efficient and manageable.

Using Debexpert for Debt Portfolio Transactions

Debexpert

Online platforms like Debexpert simplify debt portfolio trading by connecting buyers and sellers while offering tools tailored to the industry. Debexpert provides features such as multiple auction formats (English, Dutch, sealed-bid, and hybrid), portfolio analytics, and encrypted file sharing. These tools help agencies evaluate debt portfolios while adhering to North Carolina’s strict documentation standards.

Compliance is a key focus for Debexpert, which ensures all participants hold valid licenses issued by the North Carolina Department of Insurance. This is crucial in a state where operating without proper licensing is a Class I felony. North Carolina considers debt buyers to be collection agencies, meaning they must meet full licensure requirements. The platform supports trading in various types of debt common in the state, including credit card balances, auto loans, consumer loans, and medical bills.

"A 'debt buyer' means a person or entity that is engaged in the business of purchasing delinquent or charged-off consumer loans or consumer credit accounts, or other delinquent consumer debt for collection purposes." – North Carolina General Statute § 58-70-15

Debexpert also ensures secure communication through real-time chat and encrypted file sharing, which helps agencies meet North Carolina’s recordkeeping standards. These features, combined with its compliance tools, make it easier for agencies to price portfolios accurately and meet legal requirements.

Benefits of Debexpert for North Carolina Agencies

Debexpert’s analytics play a crucial role in helping agencies price debt portfolios while staying compliant with North Carolina’s regulations. For example, the platform’s filtering tools help agencies avoid acquiring time-barred debt, which is particularly important given the state’s 3-year statute of limitations for open accounts and written contracts.

The platform also supports documentation compliance under G.S. 58-70-115, which mandates that debt buyers hold proper ownership documentation and verify debt amounts before initiating collection efforts. With Debexpert, agencies can securely manage documents to ensure they have the original creditor’s name, account numbers, and itemized accounting for each portfolio. This is especially critical for meeting pre-litigation requirements, such as providing a 30-day written notice of intent to file legal action, which must include detailed account information.

Additionally, Debexpert’s tracking tools help agencies manage mandatory notices and maintain financial transparency as required by state law. This includes operating separate trust accounts and maintaining surety bonds ranging from $10,000 to $30,000. Before finalizing any transaction, agencies can use the platform’s auditing features to verify compliance with NC G.S. 58-70-50, which requires that all debtor correspondence include the agency’s true name, address, and permit number. By offering these capabilities, Debexpert minimizes the risk of acquiring non-compliant debt portfolios and ensures smoother operations for North Carolina agencies.

Conclusion

Success in debt collection within North Carolina hinges on adhering to legal requirements and maintaining ethical practices. The regulatory framework, which includes the North Carolina Collection Agency Act, North Carolina Debt Collection Act, Consumer Economic Protection Act of 2009, and the Fair Debt Collection Practices Act, sets clear standards for the industry. Starting July 1, 2024, all agencies must include their North Carolina Permit Number on correspondence, ensuring greater transparency.

Ethical operations are not just a legal necessity but a cornerstone of effective debt recovery. The Federal Trade Commission (FTC) emphasizes this, stating: "Means other than misrepresentation or other abusive debt collection practices are available for the effective collection of debts". Adhering to these principles fosters trust between creditors and debtors while avoiding penalties, which can range from $500 to $4,000 per violation.

Understanding the statute of limitations is equally important. In North Carolina, the timeframe for collecting on credit card debt, medical bills, and open accounts is only three years. Attempting to recover debts beyond this period is illegal and can lead to statutory damages. Moreover, even a partial payment or acknowledgment of the debt can restart the limitations period, making compliance with these rules essential.

Technology plays a pivotal role in meeting North Carolina's stringent documentation standards. Agencies must secure valid proof of debt ownership, itemized account statements, and maintain secure records to comply with NC G.S. 58-70-115. Automated platforms simplify this process by ensuring all documentation meets state requirements, tracking mandatory 30-day notices, and managing trust account deposits within two banking days. These systems not only help agencies avoid severe penalties, such as Class I felony charges for non-compliance, but also improve recovery rates by promoting better organization and transparency. Ultimately, leveraging technology is key to staying compliant and achieving success in debt collection.

FAQs

How can I verify a North Carolina collection agency is properly licensed?

To ensure a collection agency in North Carolina is operating legally, you can verify their license through the North Carolina Department of Insurance. Under G.S. 58-70-15, collection agencies are required to obtain a permit. You can check their license status by visiting the North Carolina License Management System or reaching out to the department directly for help.

What should I do if a collector contacts me about a debt that’s past the statute of limitations?

If a debt collector contacts you about a debt that's past the statute of limitations, you have options. You can request validation of the debt or dispute it if you believe it's inaccurate. If a collector attempts legal action on such a debt, you have the right to file a motion to dismiss the case.

In North Carolina, debt collectors are prohibited from using unfair or deceptive practices to collect on time-barred debts. If you experience any illegal behavior, make sure to report it to the appropriate authorities.

Does paying even a small amount restart the statute of limitations in North Carolina?

In North Carolina, making a partial payment on a debt does not reset the statute of limitations. The three-year limitations period stays fixed, beginning from the date the debt initially became delinquent, no matter if small payments are made later.