When businesses face unpaid invoices, they often turn to debt collection agencies. The cost of these services depends on two main pricing models:

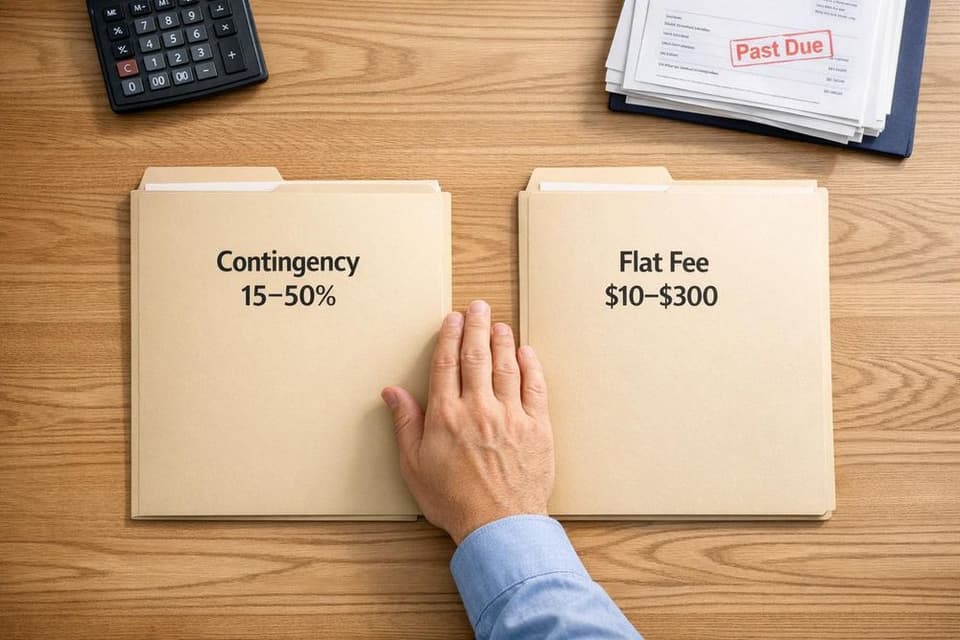

- Contingency Fee Model: You pay only if the agency successfully collects the debt. Fees range from 15% to 50% of the recovered amount, depending on factors like the debt's age and complexity. This model is ideal for older or disputed debts, as the agency takes on the financial risk.

- Flat Fee Model: You pay a fixed upfront fee per account, typically $10 to $300, regardless of the outcome. This option works best for newer debts (under 90 days old) and high volumes of small balances.

Key considerations:

- Time sensitivity: Delayed collection reduces a debt’s value by 0.5%–1% daily.

- Net recovery matters: The model that recovers the most funds - not just the lowest fee - is often the better choice.

- Hidden costs: Watch for extra fees like court filings or skip-tracing charges.

For the best results, many businesses use a combination of both models, starting with flat fees for newer debts and switching to contingency fees for tougher cases.

Contingency vs Flat Fee Debt Collection Models Comparison

Contingency vs Flat Fee Debt Collection Models Comparison

1. Contingency Fee Model

Pricing Structure

Under the contingency fee model, agencies earn their fees only when they successfully recover debt. If no debt is collected, you won’t owe anything. The fee is calculated as a percentage of the amount recovered, typically falling between 15% and 50% depending on factors like the debt's age, balance size, volume, and legal complexities.

For example:

- Newer B2B accounts (under 90 days old) often have lower fees, around 10% to 25%.

- Debts aged 90 days to one year may incur fees of 25% to 40%.

- Older debts (over one year) can see fees rise to 30% to 50%.

Smaller balances, such as those under $500, tend to have higher fees - around 35% to 45% - due to the effort required compared to the revenue generated. On the other hand, large balances over $10,000 may qualify for reduced rates, typically 20% to 30%. If legal action is required, rates can climb to 40% to 50%, especially when attorneys get involved.

These fee structures help businesses determine whether this model aligns with their needs.

Use Cases

The contingency model works well for businesses looking to avoid upfront costs. It’s particularly suited to accounts that are older (over 90 days), disputed, or require additional efforts like skip-tracing or legal action. Industries such as trucking, logistics, construction, and wholesale distribution often benefit, as they typically deal with larger debts. This model is also ideal for companies with limited billing resources or cash flow issues, as there are no upfront or recurring fees involved.

Another advantage? Agencies are motivated to tackle even the most challenging cases, especially when internal collection efforts have hit a dead end.

Advantages

One of the biggest perks of the contingency model is that you don’t pay unless the agency recovers the debt. This eliminates upfront costs and aligns the agency’s goals with your own. As Southwest Recovery Services puts it:

"This model aligns the agency's interests directly with yours. They succeed only when you do, which means they're motivated to recover as much as possible while handling accounts professionally."

Professional collection agencies often achieve recovery rates of 30% to 70% for commercial debts, a performance that can far exceed internal collection efforts. Plus, outsourcing collections allows you to maintain a professional relationship with your clients while the agency handles the tougher conversations and tactics.

Disadvantages

While the contingency model has clear benefits, there are some downsides to consider. The most obvious is the higher cost once a debt is successfully recovered. For older or more complex debts, fees can reach 40% to 50% of the recovered amount.

Additionally, there may be extra costs involved, especially when litigation is required. These can include:

- Court filing fees: $100–$400

- Process server fees: $40–$200

- Skip-tracing fees: $50 or more

Such expenses can stack up, particularly if the case involves a court judgment, a debtor with no forwarding address, or an account that’s already been handled by another agency. While these costs are sometimes unavoidable, they’re worth factoring into your decision.

2. Flat Fee Model

The flat fee model, like the contingency fee approach, focuses on balancing cost control with the potential for recovering debts.

Pricing Structure

With this model, agencies charge a fixed rate per account, paid upfront, allowing you to keep 100% of the recovered funds. Rates vary depending on the volume of accounts and the level of service required. Typical fees range from $10 to $50 per account. For high-volume clients, rates can drop to $9 to $14.50 per account, while more intensive services may cost between $50 and $300 per account. Some agencies also offer bundle pricing, such as $500 for 25 collection calls or $800 for 150 collection letters.

Use Cases

The flat fee model works particularly well for early-stage debts and portfolios with a high volume of low-balance accounts, typically ranging from $100 to $1,000. Industries like subscription services, medical practices, property management, and e-commerce often favor this model because they manage numerous small accounts. For instance, in late 2025, an Ohio dental practice used a flat fee program for 220 early-stage accounts, paying about $20 per account. Within 45 days, they recovered $10,900 while retaining all funds.

Advantages

One of the biggest perks of the flat fee model is its predictable cost structure, which simplifies budgeting. Plus, since you keep all recovered funds, it’s a cost-effective option for smaller balances. Agencies also begin work immediately, which is critical for fresh accounts.

"For a flat ~$15, you can pursue small balances without giving up 40% of the total."

This quick action matters because debts under 90 days old typically have recovery rates of 40% to 60%. On the flip side, every day an invoice remains unpaid reduces its recoverable value by 0.5% to 1%.

Disadvantages

Despite its benefits, the flat fee model has its downsides. The most notable is that you pay the fee whether or not the debt is recovered. Additionally, the services included are usually limited to "soft" collection methods, such as demand letters, automated emails, and initial phone calls, without escalating to more aggressive actions like skip tracing or legal measures. For example, a typical plan might only cover three demand letters.

Another concern is the potential for "double charging", where agencies offer a low flat fee for basic services but later require a contingency fee for full collection efforts. Be sure to check for hidden costs, such as account placement fees, annual membership dues, or cancellation penalties.

Advantages and Disadvantages

This section dives into how contingency and flat fee models impact net recovery, highlighting their unique trade-offs. Choosing the right model depends on the type of debts you're pursuing and your comfort with financial risk.

Contingency models shine with older, harder-to-collect debts because the collection agency takes on all the financial risk. You don’t pay anything upfront, and the agency only earns a fee if they successfully recover your debt. This motivates them to use more aggressive strategies like skip tracing, phone negotiations, and even legal action. However, the trade-off is the fee - agencies often take a substantial cut of the recovered funds. For debts older than two years, success rates can dip as low as 10% to 15%, meaning the agency’s effort aligns with the risk they’re taking.

Flat fee models are ideal for newer debts where a simple nudge - like a demand letter - might be enough to secure payment. This option allows you to keep 100% of the recovered amount, with predictable costs ranging from $10 to $300 per account. The catch? You pay the fee whether or not the debt is collected. Flat fee services typically include only basic methods like automated emails and demand letters, which may not be effective for unresponsive accounts.

When deciding, it’s not just about the fee percentage - it’s about the net recovery. As NexaCollect puts it:

"The real question isn't 'Who is cheapest?' but 'Who can recover the most, safely?'"

For instance, an agency charging a 35% fee but achieving a 45% recovery rate could leave you better off than one charging 25% but recovering only 20% of debts.

Here’s a quick comparison of the two models:

| Feature | Contingency Fee Model | Flat Fee Model |

|---|---|---|

| Upfront Cost | $0 | $10–$300 per account |

| Payment Trigger | Only upon successful recovery | Paid regardless of outcome |

| Financial Risk | Taken on by the agency | Taken on by the creditor |

| Best For | Older, high-balance, or disputed debts | Early-stage, low-balance, high-volume debts |

| Recovery Share | Retain 50%–85% of recovered funds | Retain 100% of recovered funds |

| Service Intensity | High (e.g., skip tracing, legal action) | Low (e.g., demand letters, automated outreach) |

Ultimately, your choice should balance the certainty of costs with the potential for recovery - a critical element in any effective debt collection strategy.

Conclusion

Deciding between contingency and flat fee models isn’t just about finding the cheapest option - it’s about getting the best overall recovery. The right choice depends on factors like the debt’s age, balance, and your comfort with financial risk.

For debts less than 90 days old, flat fee models work well. They offer predictable costs and let you keep all recovered funds, which is perfect for managing high volumes of smaller balances. For older or disputed debts, contingency models step in as a better fit. These shift the financial risk to the agency, requiring no upfront payments. The agency only gets paid if they recover funds, typically taking 15% to 50% of the recovered amount. Here, the focus should be on the agency’s ability to recover funds rather than the percentage they charge - what matters most is how much money is ultimately brought back.

Using both models together can refine your debt recovery strategy. A waterfall approach - starting with flat fees for newer accounts and moving to contingency fees for tougher cases - helps balance predictable costs with more aggressive collection methods when needed. Be sure to check contracts carefully for any hidden fees or penalties. This strategy allows you to manage costs while maximizing recovery, giving you the tools to make smart, informed decisions about debt collection.

FAQs

How do I calculate my net recovery after collection fees and add-on costs?

To figure out your net recovery, you simply subtract the collection agency's fees and any additional costs from the total amount recovered. Most agencies operate on a contingency fee basis, which usually ranges from 20% to 50% of the recovered debt.

Here’s an example: Let’s say you recover $10,000 and the agency charges a 25% fee. The math works like this:

- Fee calculation: $10,000 × 25% = $2,500

- Net recovery: $10,000 - $2,500 = $7,500

So, in this case, your net recovery would be $7,500.

When should I switch an account from flat fee to contingency pricing?

When dealing with substantial debts, debts that are relatively recent, or when your goal is to maximize recovery, switching to contingency pricing can be a smart move. This approach ties fees directly to successful collections, ensuring you only pay when results are delivered. Plus, contingency rates are often a more cost-effective option, especially for larger or newer debts, as they help align costs with outcomes.

What contract terms should I review to avoid hidden collection charges?

When reviewing contract terms, pay close attention to details like contingency fee percentages, fees for legal actions, skip-tracing costs, and charges for process servers. Also, look out for clauses that might involve hidden expenses. Being clear on these points from the start can help you steer clear of surprise costs and maintain clarity in the debt collection process.