No, it is not illegal for a collection agency to buy debt. In fact, debt buying is a common and legal practice in the United States. Collection agencies purchase unpaid debts from original creditors, such as banks or medical providers, often at a fraction of the debt's value. Once purchased, the agency becomes the legal owner of the debt and has the right to collect the full amount owed.

However, debt buyers must follow strict federal and state laws, including the Fair Debt Collection Practices Act (FDCPA) and Fair Credit Reporting Act (FCRA). These laws regulate how debt buyers can operate, ensuring they do not harass, mislead, or violate consumers' rights. Key protections include:

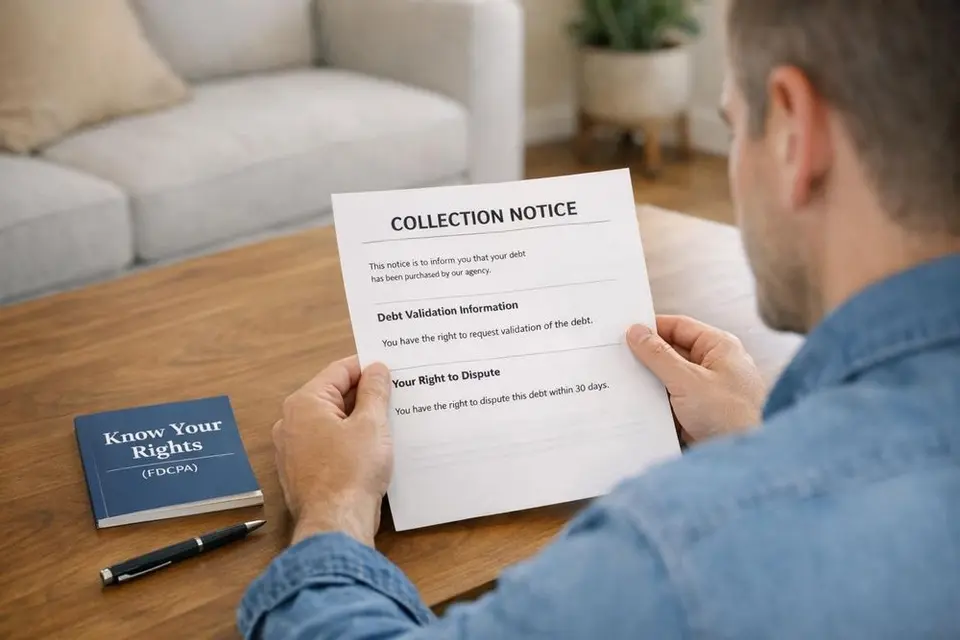

- Debt Validation: Agencies must provide written proof of the debt upon request.

- Dispute Rights: Consumers can challenge inaccuracies within 30 days.

- Communication Rules: Collectors must follow limits on call frequency and timing.

While the practice itself is legal, any abusive or deceptive collection tactics are prohibited. Knowing your rights can help you handle debt buyers confidently and avoid potential scams.

Debt Collection: Know Your Rights | Federal Trade Commission

Federal Trade Commission

Is Debt Buying Legal in the United States?

Legal vs Illegal Debt Collection Practices Under FDCPA

Legal vs Illegal Debt Collection Practices Under FDCPA

Debt buying is legal in the United States, provided collection agencies adhere to federal and state laws designed to balance the interests of creditors and the rights of consumers.

The Legal Basis for Debt Buying

Under U.S. law, debt is considered a transferable asset. Most credit agreements explicitly allow lenders to sell delinquent accounts to third parties. This practice is regulated by the Fair Debt Collection Practices Act (FDCPA), codified as 15 U.S.C. § 1692, which sets the rules for how debt buyers can operate.

According to the FDCPA, "Abusive debt collection practices contribute to the number of personal bankruptcies, to marital instability, to the loss of jobs, and to invasions of individual privacy".

The FDCPA prohibits harassment, false claims, and other unethical tactics. The Consumer Financial Protection Bureau (CFPB) enforces these rules and has introduced Regulation F, which updates FDCPA provisions to address modern communication methods like email and text messages. Additionally, the Fair Credit Reporting Act (FCRA) ensures debt buyers report accurate information to credit bureaus, allowing consumers to dispute inaccuracies. On top of federal regulations, many states have their own laws offering further protections. These frameworks help distinguish lawful debt buying from illegal collection practices.

Legal Debt Buying vs. Illegal Collection Practices

Clear guidelines exist to separate legal debt buying activities from unlawful methods. Examples of legal practices include:

- Buying debt portfolios from creditors

- Contacting debtors only between 8:00 a.m. and 9:00 p.m.

- Accurately reporting debt information to credit bureaus

- Filing lawsuits within the statute of limitations

On the other hand, illegal practices include using threats, obscene language, misrepresenting debt amounts, pretending to be government officials, or adding unauthorized fees. The FDCPA also limits collectors to no more than seven calls within a seven-day period for a specific debt. Violations of these rules can result in statutory damages of up to $1,000.

Federal Laws That Regulate Debt Buyers

Three federal laws outline the rules debt buyers must follow and protect consumers during the debt collection process.

Fair Debt Collection Practices Act (FDCPA)

Fair Debt Collection Practices Act

The FDCPA, found under 15 U.S.C. § 1692, is the main law governing how debt buyers operate. If a company's primary business involves collecting debt, they are classified as "debt collectors" under this law, even if they own the debt they collect. This designation ensures that consumer protections apply regardless of whether the debt was purchased or collected on behalf of another party.

"The Fair Debt Collection Practices Act (FDCPA) makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts." - Federal Trade Commission

The FDCPA sets strict rules for how debt buyers can interact with consumers. For example, they are limited to calling no more than seven times within seven days and must wait seven days after making contact before calling again. They cannot contact consumers outside the hours of 8:00 a.m. to 9:00 p.m., use offensive language, threaten harm, or misrepresent the debt's details or legal status. Within five days of the first contact, they must provide details validating the debt.

Violating these rules can lead to serious consequences. Consumers can sue for statutory damages of up to $1,000 per violation, plus attorney's fees. In class action cases, damages are capped at the lesser of $500,000 or 1% of the debt collector's net worth.

The FDCPA isn't the only safeguard in place. The FCRA ensures debt buyers report accurate information about your debts.

Fair Credit Reporting Act (FCRA)

The FCRA focuses on how debt buyers handle credit reporting, ensuring consumers' credit histories are accurately reflected. If a debt buyer reports your debt to credit bureaus, you have the right to dispute any inaccuracies. During a dispute, credit reporting agencies must investigate the claim, note the dispute on your report, and forward any supporting documents you provide to the debt buyer.

"If a debt collector provides or furnishes information to a consumer reporting companies that you believe is inaccurate, you have the right to dispute that information." - Consumer Financial Protection Bureau

Debt buyers are also prohibited from knowingly reporting false information. For example, if a debt is under dispute, they must disclose this status to the credit bureaus. Together, the FCRA and FDCPA work to ensure that consumers receive clear and accurate information about their debts.

The CFPB plays a key role in enforcing these laws and ensuring compliance.

Consumer Financial Protection Bureau (CFPB) Oversight

Consumer Financial Protection Bureau

The CFPB enforces debt collection laws, including the FDCPA, through Regulation F (12 CFR Part 1006), which sets modern standards for debt collection. According to the CFPB, debt buyers cannot sidestep consumer protections simply because they own the debts they collect. If their main business is debt collection, they are fully subject to FDCPA requirements.

"Regulation F implements the Fair Debt Collection Practices Act (FDCPA), prescribing Federal rules governing the activities of debt collectors, as that term is defined in the FDCPA." - Consumer Financial Protection Bureau

The CFPB monitors collection practices, enforces compliance, and provides a platform for consumers to file complaints. It also offers resources like model validation notices and guidance on using electronic communication, such as emails and text messages. Debt collectors are required to keep records of their collection activities for at least three years after their last action. If you experience abusive or deceptive behavior, filing a complaint with the CFPB can trigger enforcement actions.

While debt buying is a legitimate business, these regulations ensure consumers are shielded from harmful practices during the collection process.

Your Rights When a Collection Agency Buys Your Debt

If a collection agency takes over your debt, federal law ensures you have the same protections as before. These rights allow you to control how collectors reach out to you and give you the ability to confirm the debt’s validity before paying. These safeguards are designed to keep you informed and in control during the debt collection process.

Right to Request Debt Validation

Debt collectors are required to provide you with "validation information" either during their first communication or within five days of contacting you [6, 19]. This notice must include key details like the amount owed, the name of the current creditor, and steps to dispute the debt. Since late 2021, collectors must also include an itemized breakdown of interest, fees, and payments, along with a tear-off dispute form featuring options such as "This is not my debt" or "The amount is wrong".

"A collector has to give you 'validation information' about the debt either when they first communicate with you or within five days of the first contact." – Federal Trade Commission

If you want to dispute the debt, you must do so in writing within 30 days of receiving the validation notice. Once you take this step, the collector must pause all collection activities - this includes phone calls, lawsuits, and credit reporting updates - until they provide written proof of the debt and their authority to collect it [17, 19]. To protect yourself, send your dispute letter via certified mail with a return receipt, so you have proof it was delivered.

Right to Dispute the Debt

After receiving the validation notice, you can dispute any errors or inaccuracies in the debt. If something doesn’t seem right, submit your written dispute within the 30-day window. You can use the dispute form provided in the notice or write your own letter explaining why you’re challenging the debt. Once the collector gets your dispute, they must stop all collection efforts until they can prove the debt is valid. If they fail to do so, they are required to stop pursuing the debt and remove any related entries from your credit report.

Keep in mind that collectors assume you received their validation notice five business days after it was sent, so don’t delay your response. If a collector violates these rules, you may have the right to sue for up to $1,000 in statutory damages, plus attorney fees, within one year of the violation [6, 21].

Right to Stop Collection Calls

You also have the power to limit how often collectors contact you. To stop all communication, send a written "cease and desist" letter. Once the collector receives it, they can only contact you to confirm they’ll stop or to notify you of a legal action, such as a lawsuit [6, 20, 23]. Use certified mail with a return receipt to ensure you have proof the letter was delivered.

Even without sending a cease letter, collectors must follow strict rules about when and how often they can contact you. They can’t call before 8:00 a.m. or after 9:00 p.m. local time, and they’re limited to seven calls within a seven-day period for each debt. If you don’t want to receive calls at work, simply let the collector know - either verbally or in writing - that your employer doesn’t allow it.

| Consumer Right | Action Steps | Outcome |

|---|---|---|

| Debt Validation | Request within 30 days of first contact | Collector must provide proof of debt and verify their right to collect |

| Dispute Debt | Send a written dispute letter within 30 days | Collector must stop collection until proper verification is provided |

| Stop Contact | Send a written "cease and desist" letter | Collector must stop all contact except for legally required notifications |

Common Myths About Debt Buying

The debt buying industry is often misunderstood, leading to confusion about consumer rights and protections. Despite clear regulatory frameworks, several myths about debt buying continue to circulate. Let’s break down some of the most common ones to shed light on the facts.

Myth: Debt Buyers Can Operate Without Rules

This is simply not true. Debt buyers are held to strict standards under both federal and state laws. Key regulations like the Fair Debt Collection Practices Act (FDCPA) and Fair Credit Reporting Act (FCRA) ensure that debt buyers cannot engage in harassment, deception, or misleading practices. Regulation F has also modernized these standards, further protecting consumers.

"A debt buyer is subject to the FDCPA if either their principal business purpose is debt collection or they regularly collect debts owed to others." – Amy Loftsgordon, Attorney

If a debt buyer violates these laws, you could recover up to $1,000 in statutory damages, plus attorney fees and court costs. In class-action cases, collectors may face penalties of up to $500,000 or 1% of their net worth.

Myth: Sold Debts Are No Longer Valid

This is a misconception. When a creditor sells your debt, the legal responsibility doesn’t vanish - it simply transfers to the debt buyer. The buyer steps into the creditor’s shoes, assuming the rights and obligations tied to the original agreement. This means that terms like interest rates and fees typically remain unchanged.

"The practice of buying and collecting debt is entirely legal and regulated by several important laws designed to protect consumers from abusive practices." – JG Wentworth

Debt buyers are also required to follow all applicable laws, including providing proper validation notices and honoring your right to dispute the debt.

Myth: You Lose Your Rights When Debt Is Sold

This couldn’t be further from the truth. Your consumer protections remain fully intact, even after your debt changes hands. The FDCPA ensures that your rights are safeguarded regardless of who owns the debt. If a debt buyer violates these rights, you have the same legal recourse as you would against the original creditor.

Understanding these myths can help you navigate the debt buying process more confidently and ensure your rights are always protected.

What to Do When a Debt Buyer Contacts You

When a debt buyer reaches out, it's important to handle the situation carefully to safeguard your rights. Avoid making any payments until you've confirmed all the details and have proper documentation.

Verify the Debt Is Legitimate

The first step is to confirm that the debt is real and that the collector has the legal right to collect it. According to the Fair Debt Collection Practices Act (FDCPA), collectors are required to send a written validation notice within five days of their first contact. This notice should include key details like the debt amount, the names of both the current and original creditors, and your right to dispute the debt within 30 days.

"One of the most powerful tools you have under the FDCPA is to require that a debt collector verify the amount and validity of the debt it's trying to collect."

- Amy Loftsgordon, Attorney

If the collector contacts you before providing this notice, request it immediately. Once you receive it, review the document for a detailed breakdown of charges, including interest, fees, and payments. If you notice any errors, send a certified letter disputing the debt within 30 days. The collector must then stop collection efforts until they provide verification, including proof that they legally own the debt. Additionally, check your credit reports from Equifax, Experian, and TransUnion for any signs of "re-aging", where a debt is incorrectly reported as newer than it actually is.

After confirming the debt is valid, the next step is to determine whether it’s still legally enforceable.

Check the Statute of Limitations

The statute of limitations sets a time limit for how long a creditor or debt buyer can sue you to collect a debt. In most states, this period ranges from three to six years, starting from your last payment or the date you first missed a payment [28,29]. Once this window closes, the debt becomes "time-barred", meaning collectors can no longer sue or threaten legal action.

"A debt doesn't generally expire or disappear until it's paid, but in many states, there may be a time limit on how long creditors or debt collectors can use legal action to collect a debt."

- Consumer Financial Protection Bureau

To check if your debt is time-barred, verify the date of your last payment or when the account first went delinquent. You can also ask the debt collector directly if the statute of limitations has expired; under the FDCPA, they are required to provide an honest answer. Be cautious, though - making even a small payment or acknowledging the debt in writing can restart the clock in some states. While collectors can still contact you about a time-barred debt, they cannot take legal action. If you are sued for an old debt, be sure to use the statute of limitations as a defense.

Once you've verified the debt's legitimacy and legal status, you can move on to resolving it.

Negotiate a Settlement or Payment Plan

After confirming that the debt is valid and within the statute of limitations, you can negotiate a settlement or payment plan. Start by assessing your financial situation to determine what you can reasonably afford. Whether you're considering a lump-sum payment or a payment plan, review your income and expenses carefully. Debt buyers often prefer lump-sum settlements and may agree to accept less than the full amount. On average, settlements are around 48% of the original balance. If offering a lump sum, consider starting with an offer between 20% and 33% of the total debt. For payment plans, negotiate the total payoff amount first before discussing installment terms.

Always get any agreement in writing. The document should outline the terms, including the collector's commitment to stop collection activities and mark the debt as "paid in full" or "paid as agreed." Make sure you also receive written confirmation of payment terms and any updates to your credit report.

"Find a number you're comfortable with and say, 'this is what I can afford to give you,' period. They can take or leave it, it's your choice and not theirs."

- Shai Goldstein, Chief of A2Z Filings

Avoid giving collectors direct access to your bank account or sending post-dated checks. Instead, use safer options like money orders or checks - but only after you have a written agreement. If you're dealing with multiple debts through the same agency, you have the right to direct payments to specific debts, and collectors cannot apply payments to debts you're disputing. Lastly, steer clear of third-party debt settlement companies that charge high upfront fees. It's often better to negotiate directly with the collector or consult a reputable non-profit credit counselor.

Conclusion

Debt buying is permitted in the United States, provided collection agencies adhere to federal laws like the Fair Debt Collection Practices Act (FDCPA) and the Consumer Financial Protection Bureau's Regulation F. These rules create a balance, allowing debt purchasing while safeguarding consumers from harmful practices. For instance, debt buyers must validate debts within five days and follow strict communication guidelines.

Knowing your rights is key. You can request validation, dispute inaccuracies, or stop unwanted contact, which forces a pause in collection efforts until proper documentation is provided. These protections ensure transparency and give you legal options if agencies fail to comply.

"It is the purpose of this subchapter to eliminate abusive debt collection practices by debt collectors, to insure that those debt collectors who refrain from using abusive debt collection practices are not competitively disadvantaged, and to promote consistent State action to protect consumers against debt collection abuses."

- Fair Debt Collection Practices Act, Section 802

Legal cases, like Tepper v. Amos Financial, LLC (August 2018), emphasize that debt buyers cannot sidestep FDCPA regulations by claiming ownership of the debt. This framework not only regulates debt buyers but also empowers you to approach debt resolution with clarity and confidence.

Whether you're a consumer or an industry professional, understanding these laws helps you verify debts, check statutes of limitations, and negotiate from a position of knowledge.

FAQs

How can I tell if a debt buyer really owns my debt?

To determine if a debt buyer owns your debt, you can request a written validation of the debt. Collectors are legally required to provide this within five days of reaching out to you. Another step is to review your credit report to verify if the debt aligns with either the original creditor or the debt buyer. This helps confirm that the debt is accurately documented and connected to the right party.

Can a debt buyer sue me for an old debt?

Yes, a debt buyer has the right to sue you for an old debt as long as it falls within the statute of limitations. However, if the debt is considered time-barred - meaning the statute of limitations has expired - the Fair Debt Collection Practices Act (FDCPA) prohibits them from suing or even threatening to sue to collect it. Knowing whether your debt is still within the statute of limitations is key to understanding and protecting your rights.

What should I do if a debt buyer reports wrong info to my credit?

If a debt buyer submits inaccurate information to your credit report, you have the right to dispute it with the credit reporting agencies. To do this, provide supporting documentation that highlights the inaccuracies and clearly explain what’s incorrect. Once you file a dispute, the agencies are required to investigate - usually within 30 days - and correct any confirmed errors.

The Fair Debt Collection Practices Act (FDCPA) is in place to protect consumers from false or misleading credit reporting. This law ensures that your rights are safeguarded throughout the dispute process, holding debt buyers accountable for providing accurate information.